Independent Livestock Analyst, Simon Quilty of Global Agri Trends shares his forecast for sheep prices over the short and long term.

In March last year, I outlined my forecasts for Australian trade lamb for the next two years, based on a combination of tighter supplies and strong global demand.

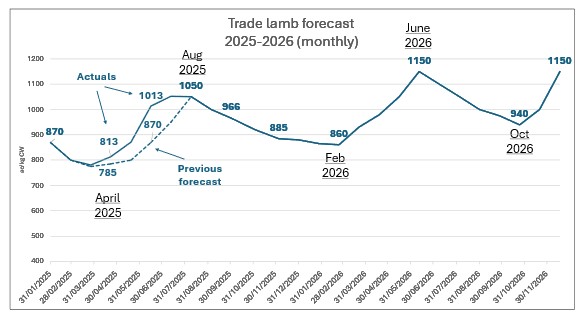

What I did not foresee was how quickly these forecasts would occur, with prices rising a month earlier than expected, driven mainly by strong global demand. Today, trade lamb prices have reached 1,050 ac/kg nationally and may still move higher to 1,150 ac/kg in August before retreating due to seasonal supply.

Line graph showing the trade lamb forecast month on month for 2025 to 2026. Source: NLRS/GAT.

Line graph showing the trade lamb forecast month on month for 2025 to 2026. Source: NLRS/GAT.

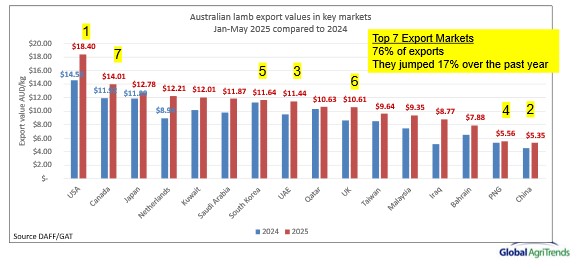

As demonstrated by the graph below, it’s the strong global demand that has driven prices to rise earlier than expected. This is despite the backdrop of the Middle East conflict. In the first five months of this year, when focusing on Australia’s top seven lamb markets, which take 76 per cent (pc) of all lamb exports, Australian lamb export values have increased by 17 pc compared to the same period last year. The US market, being the largest destination, takes the highest valued items, such as racks, shanks, shoulders, and legs, and has seen an increase in value of 26 pc. This market alone has driven the strength in heavy lamb prices.

Graph showing global lamb price rising with the top seven export markets highlighted. Source: DAFF/ GAF.

Graph showing global lamb price rising with the top seven export markets highlighted. Source: DAFF/ GAF.

Why this success story is likely to continue is that the real impact of tight sheepmeat supplies has yet to be fully realised. As we move into the winter months, there will be seasonal tightness, but it will be the coming spring and autumn that will show how truly tight sheepmeat supplies have become. As outlined in previous articles, Australia has been heavily liquidating its flock over the last two years at unprecedented levels. This has resulted in large mutton and lamb kills that will lead to shortages over the next three years and, consequently, strong livestock prices.

As stated, even with the backdrop of the Middle East conflict, sheepmeat prices have improved. One of the highlights of this year's improved Middle East demand has been Kuwait, Saudi Arabia, the UAE, and Qatar. Light lamb carcase trade has thrived in these places, at improved pricing, taking the pressure off China and other Asian markets, enabling prices to lift even with large export quantities. As a result, prices in China have improved.

The lamb story is far from over, with many more chapters to play out, with tightening supply becoming central to the plot. My forecasts of prices peaking at 11.50 ac/kg next year might be understated, but either way, a happy ending is guaranteed in 2026.

The information contained in this article is given for the purpose of providing general information only, and while Elders has exercised reasonable care, skill and diligence in its preparation, many factors (including environmental and seasonal) can impact its accuracy and currency. Accordingly, the information should not be relied upon under any circumstances and Elders assumes no liability for any loss consequently suffered. If you would like to speak to someone for tailored advice relating to any of the matters referred to in this article, please contact Elders.

More from Simon Quilty

Read other thought provoking articles from Simon, written exclusively for Livestock Now.

- Australian markets and the Middle East

- US tariffs imposed on global imports

- Threading the needle with US tariffs

- US tariffs and the Australian beef sector

- Wool & meat market forecasts amid tightening supply

- Australian cattle & sheep prices in 2024

- Brazil's fight for FMD free status

- Cattle prices -autumn 2024 forecast

- Finding the norm in global livestock prices

- Sheep prices-autumn 2024 forecast

- Meat demand from China- 2023 prediction

- Five key driver for 2023 livestock markets