The latest insights and information on the Australian sheep market as of June 2026.

Processors and exporters manage tight sheepmeat supply

Prices across the sheep and lamb complex have held relatively stable as the industry navigates its way through tight supplies and disruptions to key export markets in the Middle East.

Lamb values have largely ranged from $10.50 to 11.50/kg dressed weight (dw), while mutton prices have remained between $7.50 to 8.50/kg for most of the year. Processor demand has adjusted as prices moved out of these ranges, helping maintain generally stable values at traditionally high levels throughout autumn.

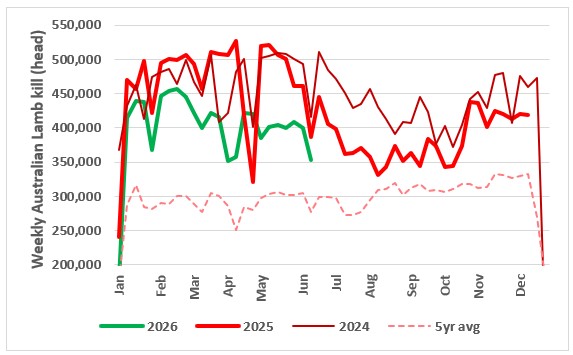

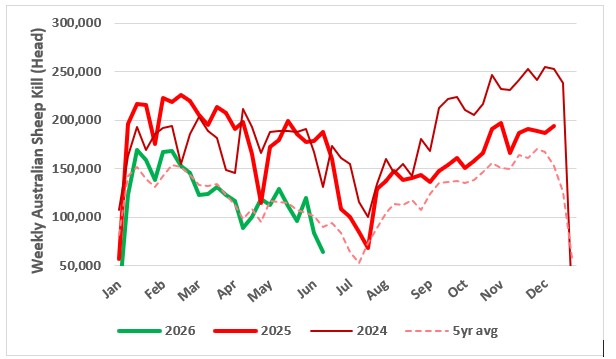

Year-to-date, the lamb kill is down 14 per cent, while the decline in production has been slightly smaller due to higher carcase weights.

Improved seasonal conditions and increased lamb feeding have enabled producers to turn off lambs at heavier weights.

This chart shows the weekly lamb kill over the past three years and the five-year average. Source: MLA.

This chart shows the weekly lamb kill over the past three years and the five-year average. Source: MLA.

Mutton kills have been even more depressed – falling 36 per cent year-to-date, as an improvement in seasonal conditions across key areas is turning producers towards rebuilding.

In terms of export performance for the year so far, although overall lamb export volumes are down by 11 per cent, Australia has increased the proportion of exports going to higher value markets:

- the United States (US) +2 per cent,

- China +4 per cent and

- United Kingdom (UK) +7 per cent.

These three countries combined with markets in the Middle East take 85 per cent of all Australian exports.

While supplies remained constrained for now, there may be some relief in sight approaching spring. Elders’ agents are reporting that that have never seen so many good, healthy lambs, feasting on some of the best fodder crops you will likely see. In southern areas where water supply has been an ongoing issue for the past 2 to 3 years, dams are slowly filling and creeks are beginning to flow as seasonal conditions turn for the better. Temperatures have remained very mild allowing pasture growth right up until the last few weeks, as frosts become heavier and more frequent.

While lamb availability will remain somewhat constrained by the heavy reduction in flock numbers over the past three years and the retention of ewe lambs for flock rebuilding, lamb supply is expected to improve this spring compared to last year. Favourable seasonal conditions are also likely to bring forward turnoff.

US market enjoying good supply of heavy lambs

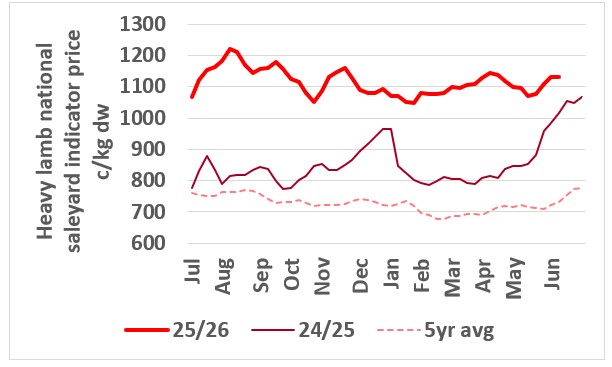

A unique quirk to this season is that there is an abundant supply of heavy weight lambs aided by increased lamb feeding and the best autumn for many years across southern Australia.

Lamb is having its moment in the US, perhaps driven by the high price of beef, and a new generation of consumers who seem to enjoy lamb as a red meat alternative to beef.

The other trend that is assisting sales into US is its focus on higher value cuts out of heavy carcases – so the US market is the least likely to see a decline in volumes over the next quarter.

Consumers in the segments that Australian lamb targets in the US are not as price sensitive as other export markets. US domestic lamb prices are averaging around 50 per cent higher than last year, and about the same amount about the five-year average as US domestic lamb supply remains in terminal decline.

Heavy lamb normally trades at equal values to supermarket or trade weight lambs, however due to the high proportion of heavy weight lambs, prices have been somewhat constrained albeit at around historic highs between $11-12/kg dw. As supplies of heavy lambs improved with the season there has been a gentle downtrend in values since this time last year.

This chart shows the national saleyard indicator prices for heavy lambs in 2024/25 vs 2025/26 and five-year average. Source: MLA.

This chart shows the national saleyard indicator prices for heavy lambs in 2024/25 vs 2025/26 and five-year average. Source: MLA.

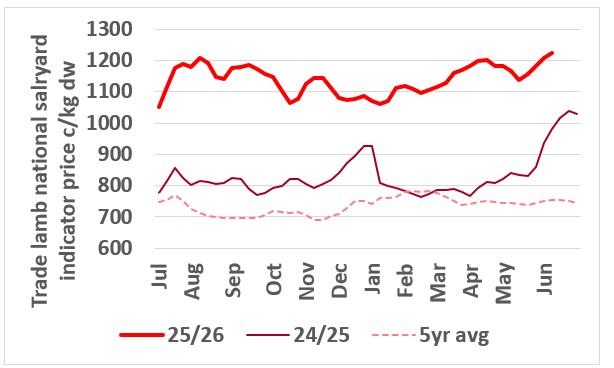

Supply tightness push trade lambs higher but consumer resistance will limit further gains

In contrast to heavy lamb categories, numbers of trade weight lambs have been proportionally lower. This, coupled with competition for local butchers from restockers and feeders has pushed prices for trade weight categories to premiums of 50 to 100c/kg premium over heavy weights, assisting a gentle rise in prices from the start of this year.

This chart shows the national saleyard indicator prices for trade lambs in 2024/25 vs 2025/26 vs five-year average. Source: MLA.

This chart shows the national saleyard indicator prices for trade lambs in 2024/25 vs 2025/26 vs five-year average. Source: MLA.

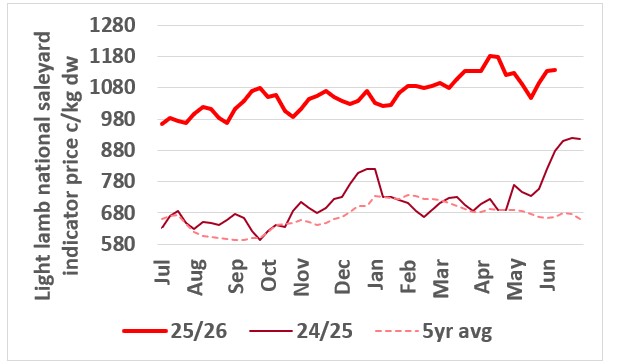

Light lambs in demand despite export difficulties into key ME markets

The emergence of a dedicated and significant lamb feeding sector, driven by three tough years across southern Australia, combined with significantly improved seasonal conditions in key lamb growing areas, has provided strong support for the light lamb market. This has helped offset disruptions to key Middle Eastern export markets arising from the US/Iran conflict.

There has been a significant drop in lamb exports to Middle Eastern markets (-36 per cent) due to high-cost relative to other proteins, disruptions to trade routes, higher freight costs and a drop off in the tourism trade through the Middle East. This has left Australian sheepmeat less competitive compared to other regional suppliers.

After a brief dip following the start of the war, light lamb prices have recovered well and will form an important part of the supply chain as the Australian lamb sector pivots to higher value export markets and generally heavier carcases produced consistently year-round, supported by. a dedicated lamb finishing sector that will operate regardless of seasonal conditions.

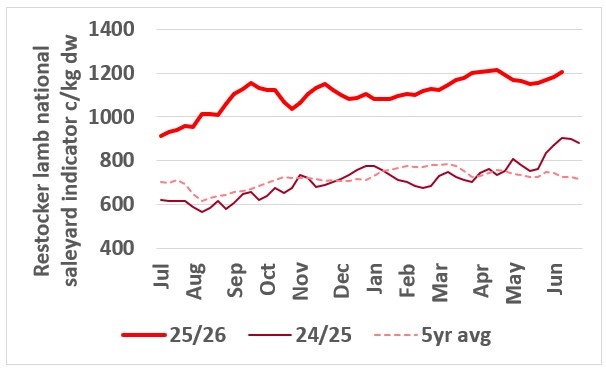

Rain breathes life into restocker market and creates options for producers

A steady improvement in seasonal conditions have made restocker lambs one of the most valuable commodities in the Australian agricultural sector. Fodder crops that look like you can walk across all through central and south-east Australia have created fierce competition for store lambs that are also in demand from a dedicated lamb feeding sector.

Reports that eastern states feeders were trying to contract western Australian store lambs at +$5/kg liveweight tells you that prices are unlikely to ease too far before the start of spring, with concerns about future supplies firmly in the mind of east coast feeders. The lift in restocker activity can be seen in interstate lamb transfer from WA to the east coast of 200,000 head for the year to May, almost double the levels of last year of 109,000 head.

This chart shows the national saleyard indicator for restocker lambs in 2024/25 vs 2025/26 and five-year average. Source: MLA.

This chart shows the national saleyard indicator for restocker lambs in 2024/25 vs 2025/26 and five-year average. Source: MLA.

Stop press:

The first new season lambs have hit the market with one agent presenting over 1,000 light weight new season sucker lambs at Wagga on Thursday. Apparently, the consignment came from Cootamundra and were February drop lambs that averaged 31kgs for $210/head, valuing them at $7/kg lw. This highlights what will be a significant change in the sheepmeat market supply dynamic with many agents thinking the next season of new season lambs could be one of the best in recent memory. Expect the lambs to come hard and early at heavier weights than ever witnessed before.

Will higher mutton prices encourage flock rebuilding?

With frequent reports of mutton sales at $9/kg dw this week, and the national average saleyard mutton indicator reaching a new all-time high >$8.50/kg dw, it’s time to consider the phenomenal recovery in mutton values – particularly when you consider they were paying 90c/kg dw three years ago (prices have lifted by a factor of 10).

The question is: does this illicit a supply response?

With an ageing demographic that have been battling against low margins for decades, finally getting a chance to make money or exit the industry on their terms, the answer is not so simple.

The economically logical answer to supernormal profits (and the reasons why we have livestock cycles) would be to build up productive capacity.

Some Elders’ agents suggest that at current prices of >$300/hd, a solid proportion of this year’s ewe lambs are heading to slaughter, with many industry stalwarts not interested in rebuilding and question marks about the preparedness of the next generation to take the job on.

Well known grazier, Nigel Kerin recently put the returns (EBIT – Earnings Before Interest and Tax) on running a sheep operation in southern NSW at $637.50/ha. Not many ag enterprises can match that, and over time this may entice a few back to the fold.

Ewe prices and lamb supply this spring will tell us whether there is any serious flock rebuilding happening.

From the rails

Read what Elders livestock representatives from around Australia are saying about the markets in their regions.

"It is one of the better autumns, we have had in the Eastern Riverina for some time."

"Good rain out in the goat country, not so much in the high stocking rate country, but certainly the pastoral areas had a good rain.

"Lambing percentages in the Riverina appear to be very healthy. We have never seen so many good, healthy lambs. So, despite the dry summer, they've managed well, fed well, and it looks like lambing percentages will be very healthy this year.

"The good thing about the Riverina is the country is well watered. With most having access to bore water or river water.

"Another agent in the central Tablelands reckons it could be the best sucker season ever with pasture conditions as good as they have seen them and the season as mild as ever, these lambs are packing on the weight and could show up as early as mid-July." - Rob Inglis, Livestock Production Manager,Vic/Riverina.

| NSW sheepmeat saleyard indicatorsc/kg dw | ||||

| 18 June 26 | +/- week | +/- month | +/- year | |

| Lambs | ||||

| Heavy | 1124 | 1134(-10) | 1068(+56) | 1047(+77) |

| Trade | 1120 | 1244(+124) | 1148(-28) | 1011(+109) |

| Light | 1115 | 1145(-30) | 1040(+75) | 911(+204) |

| Restocker | 1222 | 1337(-115) | 1153(+69) | 879(+343) |

| Merino | 1070 | 1152(+82) | 975(+95) | 823(+247) |

| Mutton | 912 | 913(-1) | 833(+79) | 670(-242) |

Source: MLA

"Some more moisture around the traps in the last week from 10-60mm, depending on what part of the state you're in. Some water has started to run into some dams, but it needs to keep raining."

"We had a frost this morning (Monday 15 June). We've been getting one a week for the last three or four weeks, but this is probably the best one we've had. So, it is getting to that time of year, where the frost will counteract what good some rain does.

"Sheep and lamb jobs flying along, it sort of bounces around from $11 to 11.50/kg. One of my clients had sheep killed at Ararat last week at $9/kg. But some works are about to go into those shutdown periods. Ararat will shut down at the end of this week, and they roll on from there." - Nick Gray, State Livestock Manager Victoria/Riverina.

"The recent surge in mutton prices is due to a shortage in supply while processors still had orders to fill. Unsure if it is sustainable with some processors going into winter maintenance, possibly for 2 to 3 weeks."

"So it might only be short-lived to a degree, but it has been at 800 to 850c/kg for a while and now it has jumped up to $9; I think it is just a true winter situation coming through.

"If a few plants start to shut down, it will be interesting if that will influence it or not.

"I don’t believe the high prices were dragging more sheep onto the market, with Bendigo’s lift in numbers this week attributed to the lack of a sale on the 8 June King’s Birthday holiday in Victoria. I don’t know whether they are there, if there any extras to drag out.

"Lamb prices have also found a new level, and some plants have no kill space available for lambs until July, while some processors have full feedlots and are stocking their pastoral country to guarantee future supplies.

"Skin values have increased, but crossbred prices varied by up to $4 between some abattoirs, and Merino skins could be worth $30-$40 depending on the wool length." - Nigel Staric, Livestock Manager, Bendigo.

| Victorian sheepmeat saleyard indicators c/kg dw | ||||

| 18 June 26 | +/- week | +/- month | +/- year | |

| Lambs | ||||

| Heavy | 1093 | 1127(+34) | 1089(+4) | 1121(+28) |

| Trade | 1190 | 1197(-7) | 1134(+54) | 1092(+98) |

| Light | 1152 | 1109(+43) | 1076(+76) | 960(+192) |

| Restocker | 1178 | 1227(-49) | 1162(+16) | 898(+280) |

| Merino | 1127 | 1088(+39) | 1013(+114) | 866(+261) |

| Mutton | 890 | 851(+39) | 808(+82) | 711(+179) |

Source: MLA

"We've had more rain over the weekend and across most of the north of the state, and a fair bit forecast. Adelaide is meant to get 3 inches of rain over the course of the next four or five days."

"Lamb job is seeing a little bit of money with up to $12/kg for trade weight lambs 18 to 24kgs, which they need to pay to compete with the store job. Most works seem $11 to $11.50/kg dw over the hooks for the short period looking into July.

"We are now Looking for some pricing into August, I think we will see a few contracts roll out because that’s when we are expecting to see supplies squeeze again.

"Mutton is off its head at $9/kg. some are saying they are making more in the yards, when you consider they were paying $9/kg dw for them three-years ago prices have lifted x 10, which is a bit scary.

"The restocker ewe job is expensive, but you have got to put it in perspective, with a reasonable season last year with a good lambing. I think there's some positive signs on the supply front and ewes are going to be at a premium going forward.

"The season is as good as we've seen for a long time. Everyone's up and about pretty much and just waiting for some pricing into that early sucker job, which I'm sure will come out in the next month." - Damien Webb, Livestock Sales Manager, South Australia.

| SA sheepmeat saleyard indicators c/kg dw | ||||

| 18 June 26 | +/- week | +/- month | +/- year | |

| Lambs | ||||

| Heavy | 1043 | 1066(-23) | 1092(-49) | 1036(+7) |

| Trade | 1117 | 1126(-9) | 1084(+33) | 1016(+101) |

| Light | 1017 | 1159(-142) | 1097(+20) | 990(+27) |

| Restocker | 1060 | 1071(-11) | 1089(-29) | 1001(+59) |

| Merino | 1035 | 1061(-26) | 1036(-1) | 880(+155) |

| Mutton | 861 | 823(+38) | 795(-66) | 618(+243) |

Source: MLA

"June has seen a notable reduction in volume through the weekly Muchea and Katanning trade sales as we push in to winter. Week of 15 to 19 June saw only just over 14,000 sheep and lambs yarded in total between Muchea and Katanning."

"Processor demand has remained strong across the mutton and lamb markets, with one major processor working hard to source numbers to complete their kill prior to their winter shutdown period. Feeder demand has also stayed strong for the better presented lines of lambs achieving rates north of $5/kg live weight on a regular basis. There has continued to be a consistent flow of feeder lambs to the South Australian and Victorian feed lotters, with the interstate transfer numbers YTD of 211,000 head vs 109,000 head last year.

"Most sheep producing areas about to commence lambing or pretty much in the thick of it now. Conception rates, lambing and early marking rates appear to be positive on the back of a solid spring and summer feed conditions. It is amazing what positive sentiment there is around the traps when prices rebound, and producers are prepared to put that bit extra back into their flocks.

"Growing season rainfall to date in parts of the Upper Great Southern area is light on and feed on the ground is still tight. Most producers still supplementary feeding some or if not all their ewe mobs." - Paul Keppel, Livestock Sales Manager, Western Australia.

| WA sheepmeat saleyard indicators c/kg dw | ||||

| 18 June 26 | +/- week | +/- month | +/- year | |

| Lambs | ||||

| Heavy | 1071 | 103(-21) | 1095(-23) | 847(+224) |

| Trade | 1121 | 1074(+47) | 1103(+18) | 860(+261) |

| Light | 1131 | 1067(+64) | 1109(+22) | 864(+267) |

| Restocker | 120 | 1111(+9) | 1124(+4) | 831(+289) |

| Merino | 1130 | 1106(+24) | 1087(+43) | 859(+271) |

| Mutton | 745 | 674(+69) | 727(+18) | 633(+112) |

Source: MLA

"We've had some more good rain go through. Virtually all of Tassie last week, anywhere from sort of 30 to 60mm, and expecting about the same over three days, which augurs well particularly for the southern part of the east coast where they need that run off to start filling some dams down there, particularly some of the dams used for irrigation. Its looking promising season wise."

"The physical lamb market for good heavy lambs is $11.20, trade weights $11.40 to $12/kg dw to average around $11.70/kg dw. Over the hooks price around $11.20/kg dw.

"Mutton $8.20 at $8.80/kg dw on the light end, $7.50 to $7.70/kg dw on the heavy end. Over the hooks $7.50/kg dw. Numbers are seasonally tight and we are just making our way to the spring to see how many come to market this year." - Gavin Coombe, Livestock Manager, Tasmania.

| TAS sheepmeat saleyard indicators c/kg dw | ||||

| 18 June 26 | +/- week | +/- month | +/- year | |

| Lambs | ||||

| Heavy | 1096 | 1121(-25) | 979(+117) | 1065(+31) |

| Trade | 1190 | 1137(+53) | 1043(+147) | 978(+202) |

| Restocker | 1193 | 995(+198) | 1067(+126) | 1025(+168) |

| Mutton | 711 | 844(+133) | 751(-40) | 730(-19) |

Source: MLA

No commentary available.

| Queensland sheepmeat saleyard indicators c/kg dw | ||||

| 18 June 26 | +/- week | +/- month | +/- year | |

| Lambs | ||||

| Heavy | 1181 | 1084(-3) | 1023(+158) | 898(+283) |

| Trade | 1131 | 1173(-42) | 1106(+25) | 848(+283) |

| Light | 1073 | 1126(-53) | 1078(-5) | 711(+362) |

| Restocker | 1000 | 1159(-159) | 826(+174) | 743(+257) |

| Mutton | 749 | 693(+56) | 654(+95) | 487(+262) |

Sources: Price data reproduced courtesy of Meat & Livestock Australia Limited.

*Disclaimer – important, please read:

The information contained in this article is given for general information purposes only, current at the time of first publication, and does not constitute professional advice. The article has been independently created by a human author using some degree of creativity through consultation with various third-party sources. Third party information has been sourced from means which Elders consider to be reliable. However, Elders has not independently verified the information and cannot guarantee its accuracy. Links or references to third party sources are provided for convenience only and do not constitute endorsement of material by third parties or any associated product or service offering. While Elders has exercised reasonable care, skill and diligence in preparation of this article, many factors including environmental/seasonal factors and market conditions can impact its accuracy and currency. The information should not be relied upon under any circumstances and, to the extent permitted by law, Elders disclaim liability for any loss or damage arising out of any reliance upon the information contained in this article. If you would like to speak to someone for tailored advice specific to your circumstances relating to any of the matters referred to in this article, please contact Elders.