The following article by our guest Brazilian correspondent Luis Vieira, looks at how the South American beef industry performed through the first quarter of 2026. Focussing on Brazil and Argentina, we discuss what to expect moving forward in the backend of 2026.

In January, we wrote the article The rise and rise of the Brazilian beef industry about the emergence of the South American cattle and beef industry and its increasing influence in global beef markets.

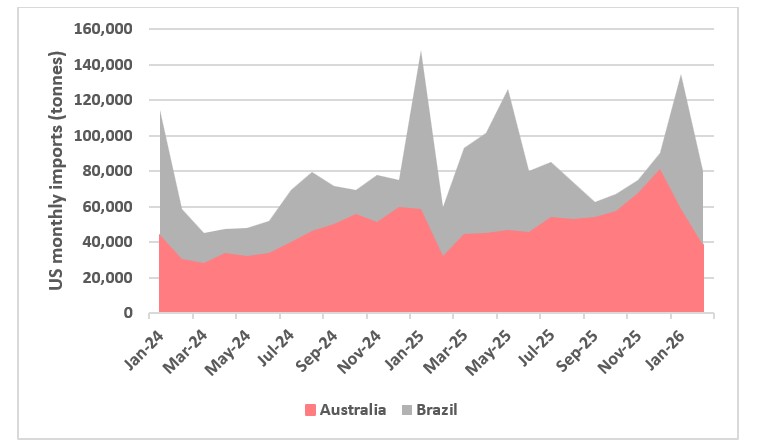

We warned that the imposition of Chinese beef import restrictions would force South American exporters to diversify its exports, pitting its beef into direct competition with Australian beef. Already, we are seeing South American beef export volumes expand into the US.

This chart shows Brazilian vs Australian beef exports to the US. Source: USDA.

This chart shows Brazilian vs Australian beef exports to the US. Source: USDA.

Improved weather supports moderate rebuilding, but slaughter levels remain strong

Through the first quarter of 2026, weather conditions across most Brazilian producing regions were generally supportive of cattle production. According to the National Institute of Meteorology (INMET), many areas in the Centre West and South received adequate rainfall, maintaining good pasture conditions. Parts of the Centre West and northern regions recorded below average rainfall, tightening local pasture availability.

These conditions supported a degree of herd retention by producers, particularly where grazing improved, but did not prevent strong slaughter activity driven by high demand. In contrast, dry conditions continued in Argentina’s Pampas region - especially in the provinces of Buenos Aires, Córdoba and Santa Fe - reducing cattle available for slaughter and reinforcing price strength.

Cattle prices

Prices paid to cattle producers in Brazil continued their upward trajectory. According to Cepea at the University of São Paulo, producer prices were 7 per cent (pc) higher year on year, and 10.7pc up in January. Average prices reached around $4.60/kg in major production centres.

Export price indices measured at Brazilian ports showed an average of $5.6/kg carcass weight, while Argentina’s export average was approximately $6.3/kg carcass weight for the same period. The comparatively higher Argentine price partly reflects persistent drought, currency instability and inflation, alongside lower cattle availability.

Chart showing Brazil's beef export price in US$ per kg comparing 2024, 2025 and 2026

Chart showing Brazil's beef export price in US$ per kg comparing 2024, 2025 and 2026

Prices in Argentina, measured by Rosario Board of Trade’s Hacienda Index, rose 17pc year on year and 11pc month on month in early 2026. Unlike the Brazilian index, the Argentine measure reflects export prices only, rather than prices paid directly to producers.

Brazil’s relative competitiveness in beef markets remained supported by its larger scale of production, lower cost structures for feed and other inputs, and the comparatively weaker Brazilian real, which sustained export competitiveness against global peers including Australia and the United States.

Brazil sets slaughter record and herd considerations

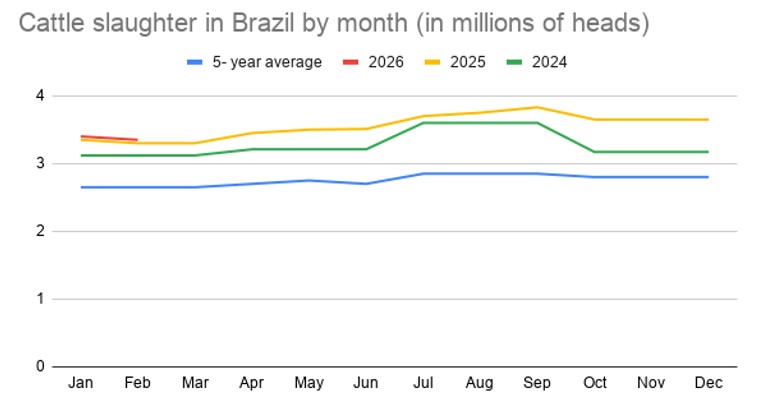

Brazil reached a new cattle slaughter milestone in 2025, processing 42.5 million head, according to official data from the Ministry of Agriculture, Livestock and Supply. Preliminary figures for January and February 2026 from major slaughter states such as Mato Grosso and Goiás indicate continued robust processing, with slaughter volumes during the first two months of 2026 at or near record monthly levels.

Chart showing cattle slaughter in Brazil by month, comparing 2024, 2025 and 2026. Source: Brazilian Institute of Economics and Statistics

Chart showing cattle slaughter in Brazil by month, comparing 2024, 2025 and 2026. Source: Brazilian Institute of Economics and Statistics

According to USDA, total slaughter for calendar 2026 is forecast at 50.2 million head. This is slightly lower than 2025, as producers begin to retain more breeding females and the cattle cycle shows early signs of inversion. This forecast reflects the expectation that herd rebuilding will slow the pace of total slaughter over the year, even as early 2026 remains elevated.

Strong demand from China has encouraged processors to maintain high processing levels, and Brazilian plants continued to pay firm prices through February. However, many industry participants expect that after the high slaughter observed in the first quarter, the emphasis will progressively shift to increased female retention as producers aim to rebuild breeding inventories.

Female slaughter and herd dynamics

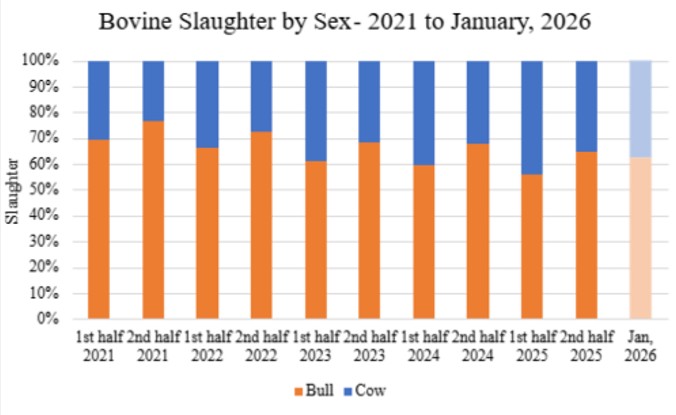

Female slaughter rates have been a key variable shaping the Brazilian cattle herd. According to USDA, cow slaughter constituted a high share of total slaughter through 2025; official Ministry of Agriculture, Livestock and Supply data suggest around 39.5pc of all slaughter in 2025 comprised cows. In January 2026, early official data show cow slaughter reduced to about 37.5pc of total slaughter, a 25pc year on year reduction in female share.

This decline is consistent with increasing producer emphasis on herd rebuilding. High female or heifer slaughter in preceding years reduced breeding capacity, and USDA analysts note that this trend should begin to taper as producers retain more cows and heifers to support future calf crops. USDA forecasts the 2026 calf crop at 47.3 million head, broadly stable with 2025, and the total cattle herd at 177.4 million head, reflecting the initial stages of cycle reversion.

Chart showing bovine slaughter by sex 2021 to 2026. Chart source: USDA FAS Brasilia using data from Brazilian Ministry of Agriculture and Livestock

Chart showing bovine slaughter by sex 2021 to 2026. Chart source: USDA FAS Brasilia using data from Brazilian Ministry of Agriculture and Livestock

Continued high slaughter volumes early in the year, coupled with a gradual reduction in female slaughter proportions, suggest that while production remains strong, the long term availability of breeding stock is tightening. This dynamic may support higher calf and replacement values as the year unfolds.

Rising input costs pressure producers

Brazilian producers have faced rising input costs entering 2026. Feed, labour, energy and transportation costs all trended higher in the early months of the year: corn prices rose about 5pc in February, diesel fuel increased around 8pc, and rural labour costs were pushed up approximately 4pc due to minimum wage adjustments. Veterinary and other production inputs also saw moderate increases.

These cost pressures have important implications for production margins, particularly as producers balance feedlot placements with pasture finishing. However, as a major global producer of corn and soybeans, Brazil retains cost advantages in feed ingredients compared to many competitors. USDA notes that total feed production in 2026 is forecast to reach 93 million tonnes, higher than 2025, with the feed industry’s capacity able to expand further if necessary.

In Argentina, rising feed costs were more pronounced during the same period, with drought exacerbating corn price pressures and increasing average feed costs by approximately 10pc in February. Elevated inflation in Argentina also fed through to diesel, energy and labour, which climbed by 9pc, 9pc and 5pc respectively.

Exports — beef and live cattle

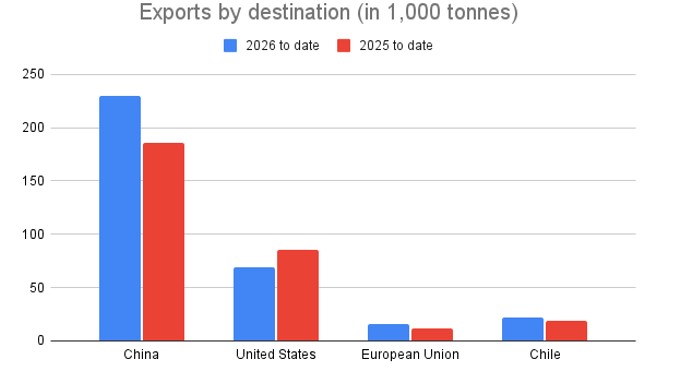

Brazilian beef exports remained strong in early 2026. According to official export records, average daily fresh beef shipments in February reached 14,820 tonnes, up 55.7pc year on year. Total exports in the first three weeks of February were nearly 192,700 tonnes, about 3pc higher than January.

Chart showing exports by destination, comparing 2025 to 2026 to date. Source: Abiec.

Chart showing exports by destination, comparing 2025 to 2026 to date. Source: Abiec.

Total export revenue for the period reached roughly $1.4 billion, with the average price per cut of fresh beef higher than recent months, driven by strong demand from China and growth in other markets.

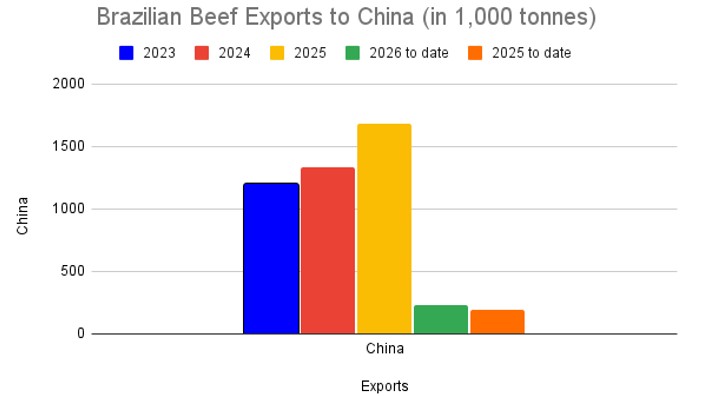

China continued to anchor Brazilian beef exports, accounting for more than 40pc of total shipments in early 2026. In November 2025, the United States reinstated a reduced tariff regime on Brazilian beef, effectively lowering tariffs to 26.4pc with a base quota of 64,000 tonnes, restoring some market access and contributing to increased shipments into early 2026.

Chart showing Brazilian beef exports to China in 1,000 tonnes, comparing 2023, 2024, 2025 and 2026 to date. Source: Abiec.

Chart showing Brazilian beef exports to China in 1,000 tonnes, comparing 2023, 2024, 2025 and 2026 to date. Source: Abiec.

Brazil also benefited from expanded access to the European Union market following its re opening to Brazilian beef and from growing demand in Africa (including Angola and Nigeria) and the Gulf States.

Live cattle exports in February 2026 totalled approximately 50,000 head, with the United Arab Emirates (around 20,000), Saudi Arabia (around 15,000) and Kuwait among the main destinations. USDA forecasts total live cattle exports in 2026 at 1.2 million head, up from about 1.05 million head in 2025, supported by continued foreign demand, particularly from the Middle East and North Africa.

Quota management and market access

China’s emerging quota management system for beef imports has become a central issue for Brazilian exporters. According to USDA, China implemented a tariff rate quota (TRQ) for beef that came into effect on 1 January 2026, allocating approximately 1.106 million tonnes of quota for Brazil. Within the quota, beef enters at a 12pc tariff, while volumes outside the quota are subject to a 55pc surcharge. The quota allocation for Brazil is only about 49pc of Brazil’s 2025 export volumes to China, suggesting that Brazilian shipments may be clipped below recent peaks unless they can be redirected into other markets.

The imposition of a safeguard TRQ in China contrasts with earlier years of largely open access and introduces a new structural variable in trade flow planning. Brazilian industry participants and USDA analysts anticipate that quota limitations will likely see some beef shipments diverted to other regions — including the United States, Middle East, Mexico and Africa — or backfilled into Mercosur partners’ domestic markets. Argentina’s allocated China quota was larger relative to its 2025 volumes (about 83.7pc of prior exports), while Uruguay’s was roughly 57.1pc.

In addition to Chinese quota constraints, Mexican trade policy also shifted. At the end of 2025, Mexico extended its Presidential Anti Inflation Decree but removed beef from duty free eligibility for non FTA partners. As a result, Brazilian beef now enters Mexico under a tariff rate quota of 70,000 tonnes, with tariff rates of 20 to 25pc applied above the quota, compared to duty free previously. This change is expected to slow export growth into Mexico unless tariff quota management can be optimised by exporters early in the year.

The recently signed Mercosur–European Union Free Trade Agreement introduced a tariff quota of 99,000 tonnes of beef annually at a 7.5pc tariff, to be phased in over five years, which should further support diversification into the EU market once ratified.

Brazilian currency and domestic demand

The Brazilian real remained relatively weak against the US dollar through early 2026, reflecting broader macroeconomic trends including inflation and export performance. According to USDA, the forecast average exchange rate for 2026 is R$5.50 to US$1.00, a level that supports export competitiveness but also increases the cost of imported inputs such as vitamins and feed additives.

Domestic beef consumption remained resilient, though price inflation for beef cuts — showed upward trends in early 2026, encouraging some lower income consumers to substitute poultry and pork for higher priced beef products.

Regional South American export trends

Argentina’s beef export performance in January and February 2026 reflected efforts to diversify markets beyond China, with shipments to Israel, Chile and Mexico increasing. Argentine exports in January totalled approximately 52,400 tonnes, generating about $189 million in revenue. China’s sporadic purchase patterns and quota developments have influenced Argentine export flows, though the country still sends more than 50pc of its exports to China.

Paraguay and Uruguay also expanded exports in early 2026. USDA forecasts Uruguay’s beef exports at around 520,000 tonnes in 2026, one of its highest levels on record, supported by steady production, established access to China, North America and Europe, and historically firm export prices.

Given its importance we plan to monitor developments across South America on a quarterly basis.

The information contained in this article is given for the purpose of providing general information only, and while Elders has exercised reasonable care, skill and diligence in its preparation, many factors (including environmental and seasonal) can impact its accuracy and currency. Accordingly, the information should not be relied upon under any circumstances and Elders assumes no liability for any loss consequently suffered. If you would like to speak to someone for tailored advice relating to any of the matters referred to in this article, please contact Elders.