Elders Business Intelligence Analyst Richard Koch discusses his data driven forecast for the Australian cattle market this spring.

The year to date

The Australian cattle industry got off to a flying start to the year with record cattle slaughter and export levels through the first quarter and cattle values gently appreciating towards record levels, particularly on slaughter and feeder categories. Store cattle were held back by the uncertain start to the year across the south and some heavy flooding across the Northern Territory and northern Queensland, which restricted cattle movements.

Underpinning the solid start to the year was strong global beef demand (mainly a result of lower than anticipated US beef production running at -6 per cent year on year) which continued to be resilient despite mounting cost of living pressures and beef’s increasingly higher relative cost to other proteins (chicken and pork). The major concern entering the year was the announcement of Chinese beef quotas on Australian beef imports, although they were expected to have little impact on prices until H2 2026.

However, the start of the autumn brought some turbulence, firstly, from hostilities in Iran which blocked trade routes into the Middle East and sent oil prices skyrocketing, increasing the cost of just about everything.

Meanwhile, producers south of the Warrego highway in Queensland, right through to Hunter Valley in NSW have been experiencing extremely dry conditions. This forced a sustained early turnoff of cattle that started with weaners and old cows and moved progressively through to pregnant females as feed and water reserves dwindled with little prospect of autumn fodder crops to get stock through winter.

Fortunately countering this was a generational weather event that brought significant proportions of rain to central pastoral areas; from the Western Australian goldfields right through north-west South Australia, Alice Springs and up to Cameron’s Corner in NSW. This coincided with an improvement in the season from Central NSW south through the Riverina (albeit a little patchy in western parts) much of South Australia and Victoria. The improvement in the season has meant that the market absorbed the NSW turnoff relatively well, although not without some price consequence, particularly on cows and heifers.

Falls in cattle prices were entirely supply driven with demand holding up well in our key export markets with year to May exports up 15 per cent driven by China (+31 per cent), Korea (+33 per cent) and the north America (+15 per cent).

The almost unprecedented early forced turnoff from NSW and southern Queensland dragged cattle values much lower than we anticipated with our forecasting skills not able to predict lowest rainfall on record for the start of 2026 in these areas. As conditions improved and turnoff slowed seasonally, cattle prices bounced back quickly to start June above forecasted levels.

The tightening in supply across the south as conditions improved and turnoff slowed seasonally was predictable, but the recent tightening in northern supplies has caught the market by surprise. Queensland producers having satisfied cash flow needs have held back cattle. This, combined with southern processors who have moved up from northern NSW to find suitable slaughter cattle to fill their seasonal supply gap over winter, has contributed to the sharp lift in cattle values since mid-May.

There are a couple of reasons for the slowing in supply out of Queensland:

- It hasn’t become cold yet

- There were cattle brought forward and killed early at 120 to 130 days off feed (rather than the normal 150-day program) to ensure they get in under the China quota which has left a bit of a gap in supply

- The high cost of restocker cattle may be encouraging Queensland graziers to hold and feed to heavier weights

- Most Queensland operations have solid financial positions

- The gap between feeders and bullocks may have gotten too tight, but

- The overriding sentiment is that they are holding to sell in July to manage their tax bills.

This has left a gap in slaughter schedules and feedlot pens for June, but agents are confident that supply pressure will ease post June with cattle being more actively booked post July.

The table below shows national saleyard averages across categories. Source: Meat and Livestock Australia (MLA) and Elders forecasts.

| Market | Apr(a) | Apr(f) | May(a) | May(f) | Jun(p) | Jun(f) |

|---|---|---|---|---|---|---|

| Heavy steer | 420 | 460 | 435 | 450 | 460 | 430 |

| Processor cows | 314 | 380 | 337 | 370 | 380 | 360 |

| Feeder steer | 456 | 480 | 471 | 470 | 497 | 460 |

| Feeder heifers | 400 | 430 | 424 | 420 | 456 | 410 |

| Restocker steer | 451 | 520 | 466 | 500 | 519 | 480 |

| Restocker heifers | 341 | 420 | 372 | 420 | 430 | 420 |

(a) Actual, (f) Forecast, (p) Projected based on sales in June so far.

Looking ahead

The upcoming season is amongst the most difficult forecasting periods I have encountered that carries a high degree of uncertainty and possible abrupt changes in supply and demand dynamics interlaced with possible significant changes in the trade landscape.

June cattle prices get ahead of themselves

Firstly, it seems some exuberance on the part of restockers and concerns about empty feedlot pens has lifted saleyard competition and overcooked cattle values. Queensland processors have also jacked up direct to works rates to attract June bookings as a warning shot that southern processors will not be getting access to cheap cattle.

At the same time, local cattle prices are surging, export beef market prices have been trending moderately lower squeezing local processing margins. Given this and the high cost of transporting cattle home from Queensland, some southern processors may opt to drop shifts or close for seasonal maintenance until local cattle availability and margins improve.

Expect to see local cattle prices ease as we head deeper into winter and cool weather starts to tease out Queensland cattle supplies. Competition from southern restockers, processors and feeders will limit the extent of price falls for northern type cattle.

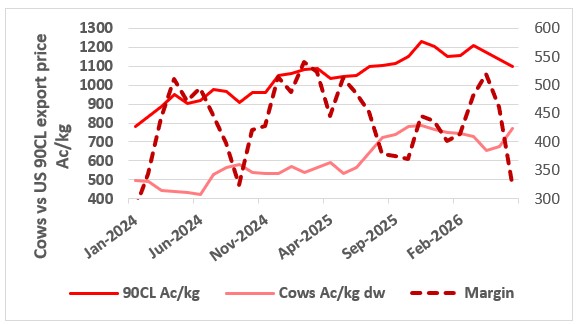

This chart shows the 90CL cow beef export price and the national average saleyard cow indicator and the margin between the two. Source: MLA.

This chart shows the 90CL cow beef export price and the national average saleyard cow indicator and the margin between the two. Source: MLA.

Premiums for Angus cattle could reach record levels this winter

The liquidation of herds through parts of southern Queensland and NSW over autumn period will have a lasting impact on supplies of southern type cattle (Angus and British cross) after herds were similarly downsized across South Australia, Victoria and southern NSW over the past 2 to3 years.

On a rough estimate, the southern breeding herd could have been reduced by 20 to 30 per cent over the past few years. This will constrain the supply of southern feeder and slaughter weight cattle for at least the next two years. The Angus/British cross feeder premiums above Queensland flatback feeders have peaked at 70c/kg Angus, with British cross 20-30c/kg lw behind.There is a further 10-20c/kg premiums for EU accredited cattle. Given the shortage of these cattle over the next few months these premiums could potentially reach record levels.

To illustrate the depth of supply concerns, feeders have been active on heifers which have increased $1/kg over the past fortnight with southern feedlots realising that traditional feeder supply areas across the New England are short and they are trying to get feeders wherever they can.

Prices for southern type stock should hold up relatively well over the winter quarter with normal seasonal supply constraints exacerbated by the early turnoff.

Price pressure to come from Queensland supplies and trade restrictions

The supply pressure will come from the north where northern producers will have heavy supplies of cattle of all descriptions available to the market from July onwards. Some of the supplies will be taken up by southern processors who will be a constant presence in these markets and keep Queensland processors honest.

The challenge to prices through the next quarter will come from changes to international trade flows as Australia and Brazil reach their Chinese import quotas. Currently Australia is sending up to 30,000 tonnes per month (21 per cent of all exports) to China and these volumes will need to be diverted to other markets (presumably at lower values) in H2 2026.

The Chinese market is now effectively closed to Australian grainfed beef, with wholesale domestic prices for grainfed cuts down more than 20 per cent, signalling early signs of market distress following Chinese restrictions.

Australia has been busy lobbying the Chinese Government for unused quota from other countries to be reallocated and for removing chilled beef and bones from quota calculations arguing that these don’t compete with Chinese domestic product.

Brazil has already filled half of its annual 1.1 million-tonne tariff-protected beef quota to China. It is on pace to exhaust the limit around mid-2026, after which any additional shipment will face a 55pc surcharge that effectively shuts down the trade with its largest customer. Industry estimates suggest that 400,000 to 600,000 tonnes of Brazilian beef will need to be redirected from China to other destinations in the second half of 2026. Live-cattle futures in São Paulo have already begun to ease as ranchers price in the coming domestic-market overhang. There is the strong likelihood that some of the displaced Chinese product will find its way to the US, intensifying competition against the Australian product.

Australia will also trigger our Korean safeguard in late July, well ahead of the September 12 date of 2025 (our above quota tariff jumps to 24pc). Previously this has been managed by placing product in bond to be used against the following year’s quota. It is uncertain if Korean importers will be willing to carry bonded product for up to five months. Last month we exported 30,000 tonnes to Korea (one of our biggest ever export months to Korea). For the year to date, 16pc of all Australian beef export exports have been sent to Korea. Like with our Chinese export volumes, some of this beef will need to be diverted to other markets.

US back into Chinese market

China has renewed the export licenses of 425 US beef plants which it let lapse in March 2025. Australian exporters have virtually replaced US beef in China which has been a key driver of our local prices in 2025 and so far in 2026. Australian exporters will be directly affected by China giving access to US beef exporters with increased in competition for grain finished product.

A further risk for Australian exporters in H2 2026 is that Trump is considering suspending the Tariff Rate Quota (TRQ) on imported beef into the US. This would allow Brazilian beef tariff free access to the US market (currently the Brazilian out of quota tariff is 26.4pc). The betting is that Trump will do something and impose a temporary additional tariff free quota. Brazil has been lobbying hard and the fact that US access to China has been restored has increased the chances of this happening, with Trump needing a win on cost-of-living pressure before the November mid-terms.

Given tight supplies of lean beef in the US, prices should hold relatively firm, however the reduction in the tariff on Brazilian beef will affect Australia’s competitive positioning in the US vs Brazilian product.

Reports are that Brazilian packers hold up to 1,000 container lots domestically, to capitalise on any change in US beef access. Most are expecting Tariff rate Quota (TRQ) duty reduction rather than full waiver, with any positive change for Brazil compromising Australia’s competitive positioning in US lean manufacturing beef markets.

Will US beef demand absorb increased imports?

A final threat to Australian beef and cattle prices over the next quarter comes with signs that robust US beef demand is starting to wane as higher fuel prices crimp shopping budgets and rising beef costs push US consumers to other proteins. Tyson Foods, a US major food company, recently released its latest quarterly results, noting that rising chicken sales helped counter a sharp drop in demand for high-priced beef. Protein-hungry but cash-strapped consumers have shifted toward buying more affordable types of meat, such as chicken and pork. Tyson Foods said beef prices climbed 11.5pc during the quarter while sales volumes sank 13.1pc.

Winter quarter will present challenges to Australian cattle prices

Don’t be fooled by the recent sharp lifts in local cattle prices. The Australian beef and cattle market is set for a difficult period in Q3 2026. Export restrictions in China and Korea take effect and a significant hike in competition from Brazilian lean frozen beef in the US manufacturing beef markets, once Brazil meets its China quota.

Cattle destined for higher quality chilled meat markets will escape most of the downturn, particularly southern types cattle and those associated with branded beef programs. However, it’s likely that there will be a general price correction across the entire local cattle market with cows and manufacturing type cattle that are destined for the US lean manufacturing fee market likely to feel most of the pain.

Cattle prices will begin to recover led by feeder cattle categories as feedlots begin buying cattle to feed for the reopening of the China market at the start of 2027.

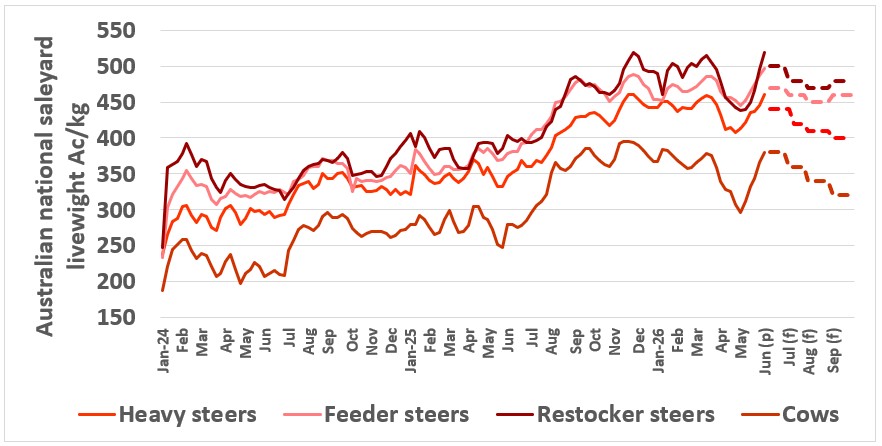

This chart shows national saleyard indicator prices and Elders price forecasts for major cattle categories. Source: Meat and Livestock Australia (MLA, Elders forecasts (f) Elders Projections (p).

This chart shows national saleyard indicator prices and Elders price forecasts for major cattle categories. Source: Meat and Livestock Australia (MLA, Elders forecasts (f) Elders Projections (p).

The table below shows the Australian saleyard indicators across categories. Source: National Livestock Reporting Service (NLRS) and Elders forecasts.

| Australian Saleyard Indicator Prices (Ac/kg lw) | |||||||

| Mar | Apr | May | Jun(p) | Jul(f) | Aug(f) | Sep(f) | |

| Heavy steer | 456 | 420 | 435 | 440 | 420 | 410 | 400 |

| Processor cows | 393 | 314 | 337 | 380 | 360 | 340 | 320 |

| Feeder steers | 489 | 456 | 471 | 470 | 460 | 450 | 460 |

| Feeder heifers | 433 | 400 | 424 | 420 | 400 | 400 | 400 |

| Restocker steer | 525 | 451 | 466 | 500 | 480 | 470 | 480 |

| Restocker heifers | 417 | 341 | 372 | 430 | 410 | 400 | 410 |

(f) Forecast, (p) Projected.

Disclaimer - important, please read:

Elders provides recommendations to the best of its knowledge and based on assumptions and information which it understands to be up to date, complete and accurate. If you are aware of any error or inaccuracy with the information on which this recommendation is based, you must immediately bring this to Elders’ attention. This recommendation is provided for your use only, and not that of any other third party. In some circumstances, the information Elders provided may be in summary form or derived from information sourced from third parties, however, Elders has not independently verified the information and cannot guarantee its accuracy.

You should always carefully evaluate all available information and consult Elders or another advisor further before you commit to any course of action or rely on any recommendation. Additionally, Elders expects that you will use your knowledge, experience and best judgement in relying on any recommendation and determining whether the recommendation is, and continues to be, appropriate. Elders do not accept liability or responsibility for any indirect, consequential or economic loss or damage of any kind arising from your acceptance or reliance on this recommendation. To the fullest extent permitted by law, all guarantees, warranties or implied terms and conditions are expressly excluded and Elders’ liability with respect to any services provided is limited to re-supply of the services, or the cost of having the services re-supplied. Elders may from time to time recommend products or services for which it may receive a financial incentive (rebate, commission, benefit, etc) from a supplier/manufacturer directly related to your purchase or use of that product or service.