Elders Business Intelligence Analyst Richard Koch discusses his data driven forecast for the Australian cattle market this autumn and the factors influencing it.

Despite a very hot and mostly dry summer and the maintenance of heavy slaughter (up 6 per cent year-on-year) and production, Australian cattle prices performed strongly through the past quarter with finished steer values leading the charge. Aiding values was tight availability of export weight cattle in the south and some logistical challenges in the north from sporadic flooding in the Northern Territory and Queensland.

The heavy steer national saleyard indicator for March is nudging record levels at 456c/kg live weight (lw). Underpinning strength in slaughter cattle values was export demand for Australian beef. For the year so far, Australian beef exports are 8 per cent higher, driven by China (up 22 per cent), Korea (up 15 per cent) and North America (up 8 per cent).

Restricted US feeder cattle supplies (ban on Mexican feeder cattle due to screwworm and lower US calf crop) is resulting in lower US cattle on feed numbers and weakening US grain-fed beef production (down 5 per cent) and higher US fed cattle prices (up 16 per cent year-on-year). This is underpinning firm global demand for Australian beef, despite the stronger Australian dollar. Solid local feedlot profitability encouraged increased feedlot capacity and high feedlot utilisation rates, ensuring firm demand for feeder steers over the summer quarter.

In comparison to other export categories, cow values struggled during the summer quarter. While export prices were firm in $US/kg as US cow slaughter remains constrained, the sharp appreciation in the Australian dollar from 64USc to above 70USc has crimped manufacturing beef export returns. These eased from A$12/kg to $11.50/kg over the quarter (but still up 10 per cent year on year), limiting the amount processors are willing to pay for cows and manufacturing cattle.

An excellent start to the northern wet season and improving conditions across the south, combined with the positive medium-term outlook for cattle prices, encouraged a step-up in restocker activity through the past quarter. Restocker heifer values remain at a hefty discount to steers at around 100c/kg lw with most southern producers favouring trading and fattening rather than herd rebuilding.

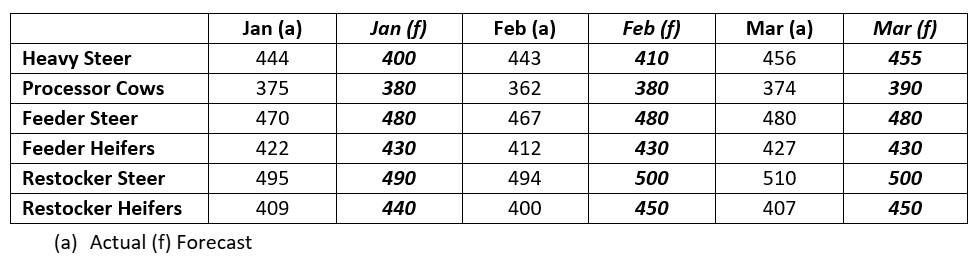

Table comparing actual and forecast Australian Saleyard Indicator Prices for the period January to March 2026. Source: Meat and Livestock Australia (MLA) and Elders forecasts.

Table comparing actual and forecast Australian Saleyard Indicator Prices for the period January to March 2026. Source: Meat and Livestock Australia (MLA) and Elders forecasts.

Prices for Australian cattle and beef will be fully firm heading into Easter with limited supplies of suitable cattle in the south and wet conditions across northern Australia and through central Queensland likely to restrict cattle movement. Only a heavy, early turnoff of cattle across northern NSW (it is very dry from Mudgee and Dubbo north through to parts of southern Queensland) and through the New England and Upper Hunter will restrict further price rises leading into Easter.

However, following Easter and as conditions in the north dry, there will be a significant step-up in northern supply. This will likely be the dominant influence in Australian cattle markets as we move through autumn, placing downward pressure on slaughter and feeder cattle values. Tightening supplies of suitable slaughter weight cattle in the south will force southern processors north to compete with Queensland works, limiting the extent of price falls. A two-speed market may prevail with prices in Queensland easing while southern values should remain relatively firm. The recent lift in fuel costs may curtail some of this activity increasing the seasonal differential between northern and southern cattle prices through autumn/winter.

The export market outlook for slaughter cattle is mixed. Lower US fed beef production will support export values for high quality chilled Australian beef exports and, therefore, heavy grain and grassfed steer prices. Higher fuel and freight costs will prove a headwind for beef demand moving forward, further stretching budgets and increasing the cost of beef for consumers. This may limit the extent of global beef price rises and local slaughter cattle values.

Increased competition in global manufacturing beef markets (as New Zealand supplies ramp up seasonally and as Brazil shifts its focus away from China to North America) will pressure lean beef values and lower prices for cattle suited for manufacturing beef markets towards the end of the quarter. Brazil is expected to fill its Chinese import quota around July/August.

A pick-up in supplies of northern feeder steers from May onwards will pressure flatback feeder steer values and widen the spread to southern feeders (Angus and Angus cross) moving the Angus premium out to up 50c/kg lw over flatbacks. Higher grain costs are tightening cattle feeding margins (grain prices have lifted from $330/t to $385/t Downs feedlot since harvest with further gains likely) and will dampen feeder cattle demand through the autumn quarter. Also, cattle placed into feedlots this autumn are likely to exit during the period where China beef import restrictions start to bite, which may further reduce feeder demand.

Restocker values will be determined by how the southern wet season plays out. While many areas are off to the best start in years, the Bureau of Meteorology (BOM) three-month outlook for April to June suggests rainfall is likely to be below average for most of Australia, with an increased chance of unusually low rainfall for parts of south-east, eastern and northern Australia.

Restocker values may moderate seasonally during the autumn quarter, particularly if fuel costs remain elevated. Heifers should narrow the wide discount to steers with northern producers expected to sell down cows and load up on lighter heifers once it dries out in the north.

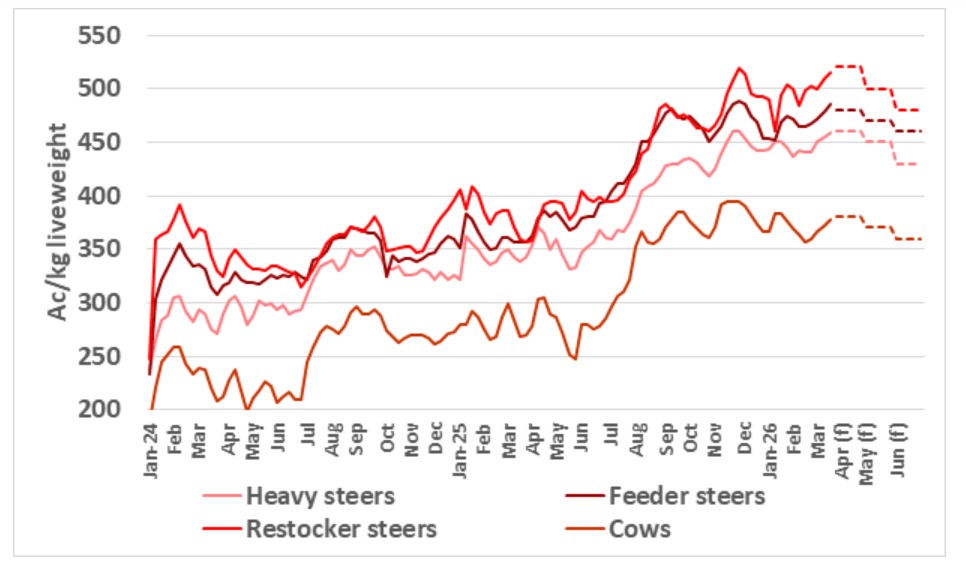

This chart shows national saleyard indicator prices and Elders price forecasts for major cattle categories. Source: Meat and Livestock Australia (MLA) and Elders forecasts (f).

This chart shows national saleyard indicator prices and Elders price forecasts for major cattle categories. Source: Meat and Livestock Australia (MLA) and Elders forecasts (f).

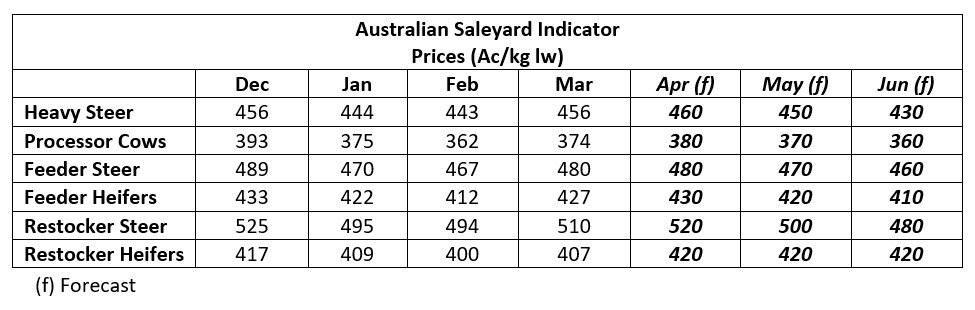

Table showing actual and forecast Australian Saleyard Indicator Prices for the period December 2025 to June 2026. Source: National Livestock Reporting Service (NLRS) and Elders forecasts.

Table showing actual and forecast Australian Saleyard Indicator Prices for the period December 2025 to June 2026. Source: National Livestock Reporting Service (NLRS) and Elders forecasts.

The information contained in this article is given for the purpose of providing general information only, and while Elders has exercised reasonable care, skill and diligence in its preparation, many factors (including environmental and seasonal) can impact its accuracy and currency. Accordingly, the information should not be relied upon under any circumstances and Elders assumes no liability for any loss consequently suffered. If you would like to speak to someone for tailored advice relating to any of the matters referred to in this article, please contact Elders.