Several factors, none of which were positive, have combined to see Australian cattle prices wobble into Easter to end a month of steady declines.

National saleyard price averages have fallen across the cattle complex from near all-time highs in mid-March:

- Heavy steers 460 to 420c/kg lw (-9 per cent),

- Processor cows 380 to 330c/kg lw (-13 per cent)

- Feeder steers 485 to 455c/kg lw (-6 per cent) and heifers 430 to 390c/kg lw (-9 per cent)

- Restocker steers 515 to 460c/kg lw (11 per cent) and heifers 405 to 350c/kg lw (-14 per cent).

The key will be US beef import demand, which has remained resilient in the face of a myriad of economic challenges, supported by lower US beef production (-8pc year to date). US demand for imported beef has underpinned the rise in global beef prices over the past few years. It will be called on to do more heavy lifting to absorb increased beef supply from Australia and Brazil, as Chinese beef import restrictions start to bite mid-year.

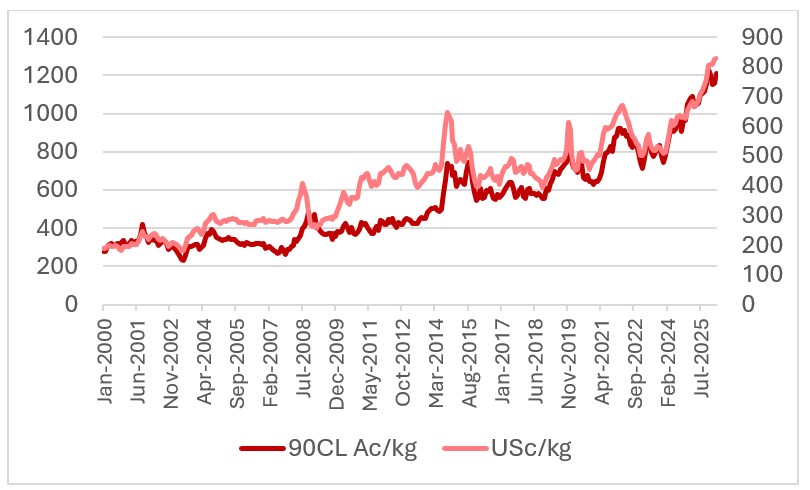

Australian beef export prices to the US continue to hold at near record levels, supported by high US domestic lean beef values and low US cow slaughter, despite increasing competition from South America.

This chart shows Australian 90CL beef export prices to the US in Ac/kg & USc/kg. Source: USDA and MLA.

This chart shows Australian 90CL beef export prices to the US in Ac/kg & USc/kg. Source: USDA and MLA.

As Queensland begins to dry out and head towards its peak turnoff season, and with looming restrictions on beef exports to China (currently our second largest export market), the local cattle market is set for a stern test over the next few months.

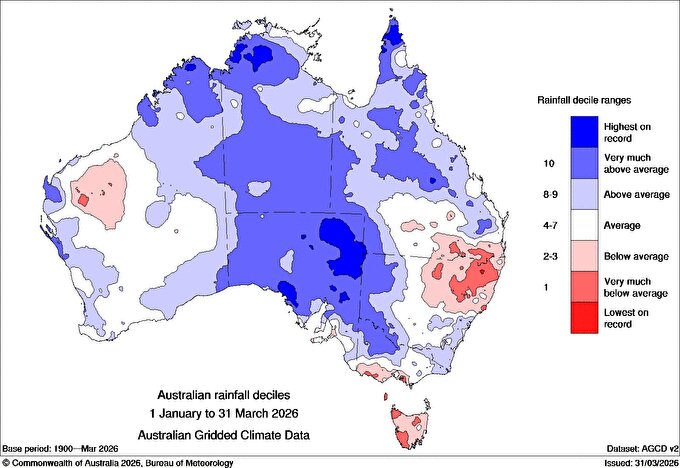

Dry conditions

It’s dry from Murrurundi in the Upper Hunter NSW to Warwick in Queensland. The New England is particularly affected, with a lack of soil moisture making it difficult for a region that relies heavily on early autumn sown fodder crops and winter pastures. Producers in affected areas have sold their culls, older stock and weaners and will move onto breeding stock without significant rain in the next four weeks.

This chart shows rainfall 1 January to March 2026. Source: Bureau of Meteorology.

This chart shows rainfall 1 January to March 2026. Source: Bureau of Meteorology.

The sell down is partly price related with many opting to take the attractive prices on offer rather than punting on a turnaround in the season. If prices continue to fall, selling pressure may ease, with producers opting to feed stock through, given the relatively attractive longer-term outlook for cattle prices.

Cash flow

Producers in Queensland are ramping up sales to generate some cash flow. Many Queensland producers have had cattle locked up and haven’t banked a cheque since late last year. A recent live export order ex Townsville at $4.20/kg for Indonesian feeder cattle filled in two days, highlighting how keen producers are to sell.

Queensland processors have a backlog of cattle heading into a run of shorter weeks – some carried over from earlier bookings that were deferred due to the wet. This has put pressure on Queensland over the hooks rates which have moved back 30-40c/kg dressed weight (dw) over the past fortnight and remain under pressure from increasingly supply.

Grain prices

Grain prices have moved +$50/t in the past fortnight to $400/t & $415/t Downs for wheat and barley respectively. This has placed pressure on feedlot margins and demand for feeder cattle. Flatback feeder quotes have moved back sharply (from 485 to 460c/kg lw) as Queensland supplies ramp up; southern feeders (Angus/BritishX) were less affected as supply of these cattle types tightens seasonally. Premiums on southern feeders have moved to 45c/kg for Angus and to 25c/kg lw BritishX.

If flatback feeder values continue to fall to near finished cattle values, Queensland producers with feed reserves may choose to hold cattle till post June once initial cash flow needs have been met.

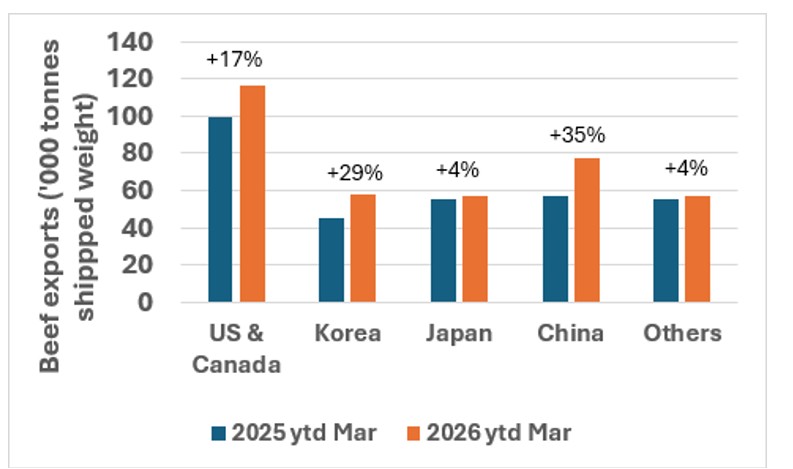

China focus

Processors are ramping up kills on cattle for China as they try and push beef in ahead of import restrictions. This is affecting demand for other cattle types, particularly cows in northern works, but also secondary cattle types as processors become more discerning about kill composition as supply increases.

Chinese quota

As at the end of March, it is estimated that Australia has filled around 50pc of its Chinese quota which suggests we will trigger safeguard restrictions (55pc above quota tariff) around mid-year. Buying from north Asia has slowed in anticipation of a weakening in prices once Australia has filled its Chinese quota. Trade sources indicate rather than paying the 55pc above quota safeguard tariff, Chinese consumers will shift beef consumption to pork/poultry.

This chart shows Australian beef export volumes to major markets. Source: DAFF.

This chart shows Australian beef export volumes to major markets. Source: DAFF.

Softening in domestic wholesale market

Media has been reporting that there have been some significant falls in domestic wholesale beef prices in recent weeks, particularly on higher value cuts/items. Partly this is related to the impact of high fuel costs on shopping budgets. It is also due a weakening in domestic wholesale demand on the expectation of an easing in prices once Australia triggers its Chinese beef quota.

Domestic wholesalers are reporting a move to cheaper items and away from grainfed and Wagyu. Retail sale volumes were reportedly notably softer in the leadup in Easter this year.

Also impacting local wholesale markets, is the loss of the Middle East market for high quality beef which is now being priced into other markets. Australian beef export volumes to the Middle East have halved since the start of war in the Middle East.

Fuel and freight costs

The cost to freight cows from Morven in Queensland to Victoria is now approx $280/head or 45c/kg, compared to 30c/kg lw or $180/head just six weeks ago. Competition from southern processors for cows in the northern markets to truck back for processing has supported northern cow values over the past 12 months.

Increased freight costs are now working through the supply chain, leading to a reduction in cow prices and an increased spread between northern and southern cow values.

Higher freight costs appear to be taking a toll on restocker cattle demand which has withered over the past month as fuel prices skyrocketed and the price of trucking cattle has lifted significantly.

Some processors have moved to place a fuel surcharge on beef deliveries to wholesale customers. This has never been seen before and will need to be absorbed somewhere through the supply chain. These same pressures are being felt in supply chains globally and unless these costs can be passed onto consumers (possible), they will need to be absorbed somewhere in the supply chain (most likely through lower cattle prices).

Looking ahead

The outlook over the next few months is looking increasingly difficult with several factors combining to increase downside price risks.

Disclaimer - important, please read:

Elders provides recommendations to the best of its knowledge and based on assumptions and information which it understands to be up to date, complete and accurate. If you are aware of any error or inaccuracy with the information on which this recommendation is based, you must immediately bring this to Elders’ attention. This recommendation is provided for your use only, and not that of any other third party. In some circumstances, the information Elders provided may be in summary form or derived from information sourced from third parties, however, Elders has not independently verified the information and cannot guarantee its accuracy.

You should always carefully evaluate all available information and consult Elders or another advisor further before you commit to any course of action or rely on any recommendation. Additionally, Elders expects that you will use your knowledge, experience and best judgement in relying on any recommendation and determining whether the recommendation is, and continues to be, appropriate. Elders do not accept liability or responsibility for any indirect, consequential or economic loss or damage of any kind arising from your acceptance or reliance on this recommendation. To the fullest extent permitted by law, all guarantees, warranties or implied terms and conditions are expressly excluded and Elders’ liability with respect to any services provided is limited to re-supply of the services, or the cost of having the services re-supplied. Elders may from time to time recommend products or services for which it may receive a financial incentive (rebate, commission, benefit, etc) from a supplier/manufacturer directly related to your purchase or use of that product or service.