Elders Business Intelligence Analyst Richard Koch shares his data driven forecast for the Australian sheepmeat market this summer.

Sheepmeat prices performed strongly during the spring quarter under the same influences. These include:

- a significantly lower lamb cohort because of lower ewe numbers and joinings (a result of flock liquidation in 2023 and 2024),

- poor lambing and marking percentages (due to mixed seasonal conditions)

- a move to retain ewes that has sharply restricted available sheepmeat supply.

This has resulted in prices largely retaining winter levels at historically high levels through spring.

As expected, supplies improved moderately through spring as new season lambs eventually hit the market albeit 6 to 8 weeks behind normal. Lamb values peaked around $11 to $12/kg carcase weight (cw) in early spring until the flush of new seasons lambs hit the market in October/November which saw prices ease to $10 to $11/kg cw.

Our forecasts underestimated price levels through the spring quarter by around 50c to $1/kg cw. The shortage in lamb supply has been more critical than expected. The lateness of the season was difficult to predict and subject to seasonal conditions which were very mixed for most of spring and didn’t really improve until November.

Prices into the end of the year may be affected by quality with yardings compromising a greater proportion of dry and woolly lambs from western and northern lambing areas that are showing the effects of the season, lacking weight and finish. This might be the order of the day for December with spreads between light and heavier lambs increasing until supplies out of feedlots ramp up in Q1 2026.

One of the features of this spring has been the large numbers of store conditioned lambs sold to feedlots. To generate cash flow, producers have decided to take advantage of attractive prices and turn off lambs early to feeders for around $200 to $250 per head rather than take a punt on the season and risk not being able to finish lambs to slaughter weights on pasture.

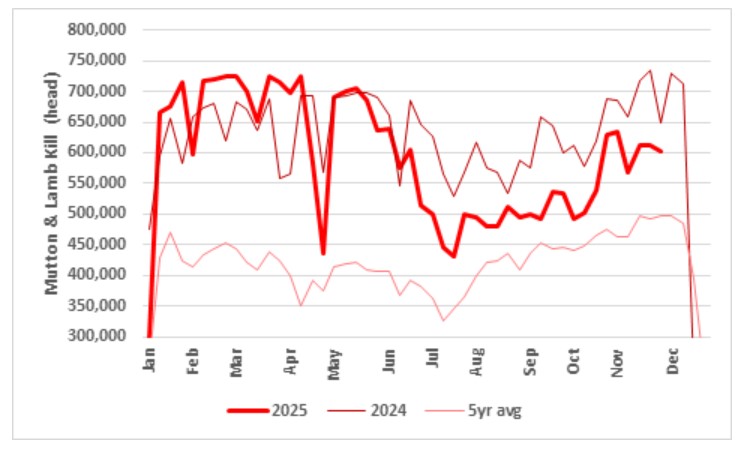

This chart shows Australian weekly sheepmeat slaughter in 2025 vs 2024 and the five-year average. Source: NLRS.

This chart shows Australian weekly sheepmeat slaughter in 2025 vs 2024 and the five-year average. Source: NLRS.

Sheepmeat exports are hanging in there, with lamb shipments down 5 per cent (lamb slaughter down 6 per cent) and mutton down 13 per cent (slaughter down 8 per cent) year to date, falling mostly in line with lower slaughter rates. Exports have shifted away from price sensitive markets in the Middle East to higher value destinations in the European Union (EU), Asia and the US.

Talking with a domestic processor, some export markets have the capacity to pay the equivalent of $10/kg dw, but it is hard to extract the same value for middle cuts (racks etc.) from the domestic market which is mainly focussed on legs and shoulders. Export sales to some markets have become more difficult as prices rise above $10/kg cw.

Forward contract prices of above $10/kg into year’s end for suitable weight slaughter lambs will underpin lamb prices at historically high levels. The major threat to current pricing levels will come from the weak processing margin environment with some works reportedly operating at around breakeven margins.

Ewe sales which provide a measure of the intent of the industry to rebuild flocks, got off to a reasonable start with much promise, the lack of spring rainfall saw demand wither and the promise of $500 per head ewes was short-lived. The results of the ewe sales could be best described as patchy with the right article (modern dual purpose merino ewe) selling to reasonable demand but others selling for not much more than meat value. As conditions improved in November, late season ewe sale results improved with a record of $540 per head paid for first cross ewes at Naracoorte blue ribbon sales. But these results were the exception and WA agents report a lack of east coast inquiry for Merino ewes which highlights that the strength of rebuild is uncertain with many still undecided about rebuilding flocks.

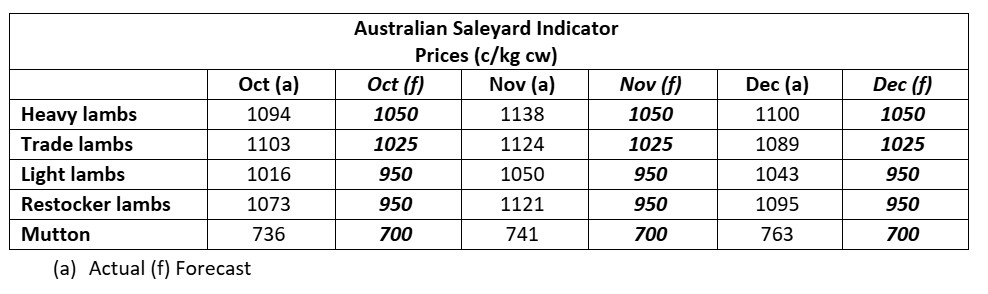

This table shows the Australian saleyard indicators across different categories of sheep. Source: Meat & Livestock Australia (MLA), Elders forecasts.

This table shows the Australian saleyard indicators across different categories of sheep. Source: Meat & Livestock Australia (MLA), Elders forecasts.

Looking forward into the summer forecast period, the smaller 2025 lamb cohort will continue to underpin sheepmeat prices at traditionally high levels. Increased availability of trade and heavy weight lambs out of feedlots through the first half of 2026 should keep lamb prices in check as will consumer resistance to high prices which may see a further decline in domestic consumption at forecast price levels.

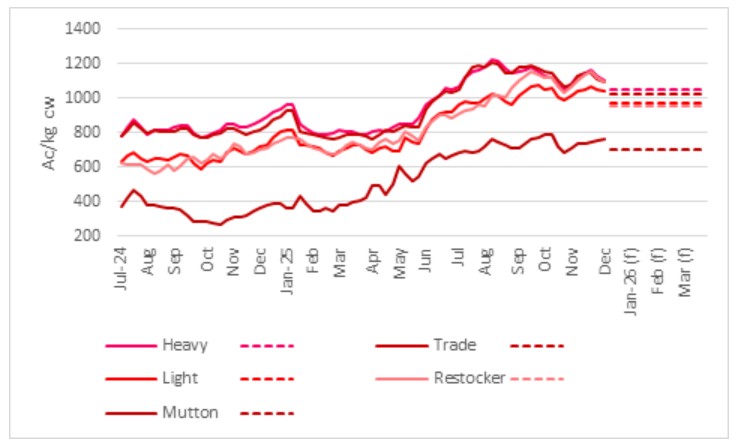

This chart shows the national saleyard indicator prices and price forecasts for major sheepmeat livestock categories in c/kg dressed weight. Source: Meat & Livestock Australia (MLA), Elders forecasts.

This chart shows the national saleyard indicator prices and price forecasts for major sheepmeat livestock categories in c/kg dressed weight. Source: Meat & Livestock Australia (MLA), Elders forecasts.

But solid export demand for Australian sheepmeat as export supplies of our major competitor NZ contract, will underpin strong prices for Australian sheepmeat through the first half of 2026. Lower production is crimping NZ exports, which fell 4.8 per cent and are forecast to fall another 1.9 per cent in the upcoming season to 357,000 tonnes - the smallest NZ export total in 15 years.

At the same time, improved market access is shifting the distribution of NZ exports. NZ signed a Free Trade Agreement with the European Union (EU) which came into effect on 1 May 2024. This has provided an increase in the tariff free quota for NZ sheepmeat into the EU. Due to this, and a shortage of sheepmeat in the EU, exports from NZ into the EU increased by 14 per cent in 2024–25 to 74,097 tonnes.

In the context of lower NZ production and increased focus on the premium EU market, NZ exports into markets outside of the EU fell by 10 per cent. NZ exports to China and the US fell by 11 and 10 per cent respectively in 2024–25, presenting an opportunity for Australian exporters to build market share in sheepmeat export markets outside the EU.

Sheepmeat supplies should improve in the second half of 2026 owing to a return to more normal lambing and marking percentages which should see lamb prices moderate from spring 2026. Higher lamb prices in 2025 should extract a supply response from the industry with more ewes joined in 2026. However, ongoing mixed seasonal conditions and the preference of the younger generation for cropping over sheep (due to the ease of management) may limit the extent of the rebuild.

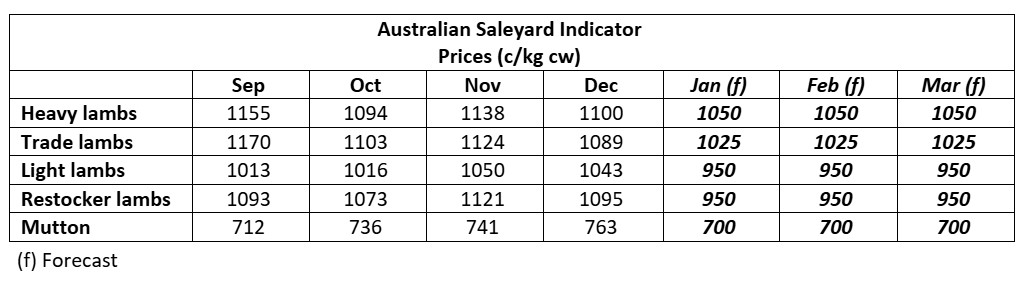

This table shows Australian saleyard indicators across different categories of sheep, including forecasts to March. Source: Meat & Livestock Australia (MLA), Elders forecasts.

This table shows Australian saleyard indicators across different categories of sheep, including forecasts to March. Source: Meat & Livestock Australia (MLA), Elders forecasts.

The information contained in this article is given for the purpose of providing general information only, and while Elders has exercised reasonable care, skill and diligence in its preparation, many factors (including environmental and seasonal) can impact its accuracy and currency. Accordingly, the information should not be relied upon under any circumstances and Elders assumes no liability for any loss consequently suffered. If you would like to speak to someone for tailored advice relating to any of the matters referred to in this article, please contact Elders.