Welcome to the Elders Insights' Weekly Market Summary for the week 27 July to 2 August 2026. We recap what’s happened on the Australian commodity markets over the past week and influencing factors.

At a glance:

- Drought declared for parts of southern Queensland

- Livestock prices continue to ease moderately, while export prices to US take another hit

- Black Sea supply issues support global grain markets

- A good week for cotton.

Weather

The Balonne, Goondiwindi and Southern Downs local government areas, along with the southern part of Maranoa in Queensland, have been declared drought-affected, after 12 months of below average rainfall. Large areas of southern and central Australia endured freezing minimum temperatures last week. This was the first decent cold spell of winter.

There was very little rainfall for most of Australia, except in southern parts of Victoria and through most of western and central Tasmania. The forecast has 10 to 25mm of rain for Western Australia, South Australia, Victoria and Tasmania, with the heaviest falls across western parts of Tasmania.

Get weather forecasts for your region on Elders Weather.

Australian Dollar

The Australian $ continues to grind higher. The US Fed kept rates unchanged at 3.75per cent last week. A split vote suggests increasing concern about inflation which raises the possibility of a September hike if incoming data remains firm. The Australian $ firmed due to a softer $US, after the Fed meeting with ongoing instability in the Middle East holding it back. Japanese Yen Intervention by the US also contributed to a softening in $US cross rates.

Livestock

Cattle markets have continued to ease moderately as local conditions turn dry, Queensland turnoff increases, and as international beef prices ease. The heaviest falls were across restocker categories as they begin to realign with slaughter cattle values. Manufacturing beef export prices to the US fell sharply last week by around 40c/kg to 11$/kg as weaker demand intersects with increased supplies out of Australia and Brazil.

Sheepmeat prices have eased by 1 to 5 per cent as processor demand weakens. Several plants have shut for seasonal maintenance while other plants work through previously contracted lambs. Drying conditions are bringing lots of goats from pastoral areas of South Australia and NSW which may impact mutton demand. Most lambs remain above $11/kg with mutton around $8.50/kg, but the trend is lower.

The big concern for livestock producers is the lack of runoff rainfall from southern Queensland through to the western district of Victoria.

View livestock for sale and our sales calendar listings.

Grain

Grain prices eased into the weekend but still recorded solid weekly gains. European production estimates continue to fall as summer crop conditions deteriorate. Black Sea exporters are trying to work out how to get grain to markets as key Black Sea routes remain closed. Until a viable solution is found international grain prices will be well supported.

Local prices continue to work higher, particularly in the northern feed zone but also across central areas of NSW with grower selling slow on dry forecasts.

For more detail, refer to the latest Cropping Market Update.

Trade your grain at your price on the secure GCX platform.

Wool

The Australian wool market is currently in its three-week recess.

Learn the many ways we support wool growers.

Cotton

International cotton futures recorded their biggest monthly rise in three months to sit at 79.65USc/lb, supported by technical buying and concerns around hot and dry weather in key US growing regions and a weaker $US. USDA weekly export sales report showed net export sales at 352,400 bales. With inventories and forward cover light, mills are prepared to buy on price dips, while 100 per cent clearance rates on sales out of Chinese state reserves are also giving comfort to the market.

Local prices are steady at $613 to $603/bale, Dalby/Moree Gin while cottonseed remains at $510/tonne.

Sugar

Raw sugar futures were lower at 14.66USc/lb after hitting a two-week low midweek, amid a more favorable harvesting outlook for top producer Brazil. Dry weather forecast in top sugar producer Brazil, will allow for a fast harvesting and processing pace. Brazilian consultancy Pecege estimated the current cane crop at 642 million metric tons (mmt), a near-record crop. Aiding prices is the uncertain outlook for Indian production with monsoon rains anticipated to be lower than average due to El Nino. Lower projected production for India and higher use of cane for ethanol has analysts expecting a sugar production deficit this year which will support prices over the longer-term.

Green Pool Commodity Specialists raised their global 2026/27 sugar deficit to -3.3mmt on Wednesday, from a June estimate of -1.76mmt. On Tuesday, StoneX raised its 2026/27 global sugar deficit forecast to -1.7mmt from a May estimate of -550,000t.

Learn about the many ways Elders helps cotton growers.

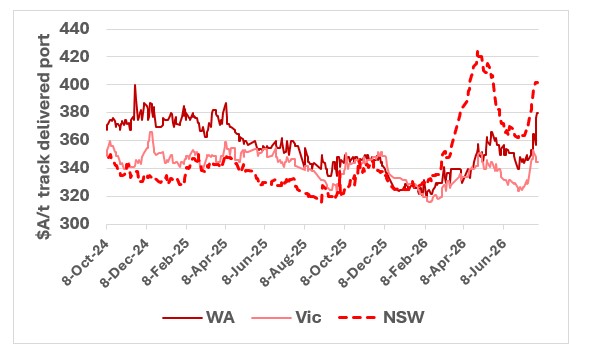

Spotlight on: grain prices

In contrast to the last rally in Apr/May that was largely inspired by dry planting conditions and higher oil prices, the most recent grain price rally is being driven by concerns around Black Sea supplies (around 35% of global exports). Russia and Ukraine have been attacking grain infrastructure across major Black Sea shipping ports which has seen some export routes shutdown.

This chart shows wheat prices at major ports in Western Australia, Victoria and NSW. Source: CGX.

This chart shows wheat prices at major ports in Western Australia, Victoria and NSW. Source: CGX.

The information contained in this article is given for the purpose of providing general information only, and while Elders has exercised reasonable care, skill and diligence in its preparation, many factors (including environmental and seasonal) can impact its accuracy and currency. Accordingly, the information should not be relied upon under any circumstances and Elders assumes no liability for any loss consequently suffered. If you would like to speak to someone for tailored advice relating to any of the matters referred to in this article, please contact Elders.