The latest insights and information on the Australian sheep market as of March 2026.

Significant widespread rain across major sheep regions will crimp supplies

A generational rainfall event through pastoral areas of South Australia and New South Wales that delivered rainfall to most of the south-east has created some processor buying urgency. This has lead to sharp rises in sheep (+7 per cent) and lamb values (+5 per cent) entering March. Lamb prices have moved to a new all-time high trading level between $11 to 12/kg dressed weight (dw) and sheep to $7 to 8/kg dw.

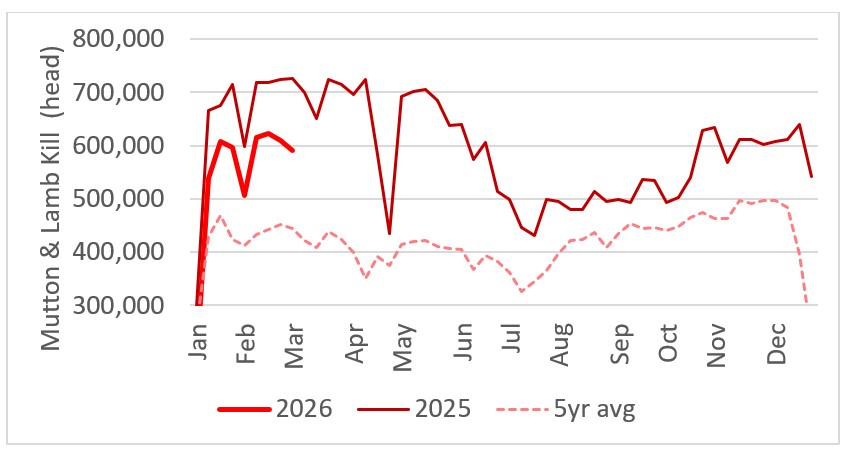

The industry is facing the full consequence of heavy flock liquidation and successive poor breeding seasons over the past three years. Slaughter and production is expected to bottom out this autumn and winter before supplies recover moderately in spring.

Sheep (-29 per cent) and lamb slaughter (-11 per cent) will tighten further seasonally over the next few months. Combined sheep and lamb slaughter last week sat at 550,000 head/week and will trend lower seasonally towards 400,000 head/week during the winter months. This creates supply challenges for processors.

Chart shows combined lamb and mutton kill 2025 vs 2026 and 5year average. Source: MLA

Chart shows combined lamb and mutton kill 2025 vs 2026 and 5year average. Source: MLA

The export sector has done a good job of managing lower supply through its seasonal peak demand period (during the first quarter coinciding with religious celebrations - Ramadan and Greek Easter). Lamb exports for the year so far are down just (-3 per cent) while mutton exports (-29 per cent) and goat exports are down sharply (-16 per cent) in line with lower slaughter. This suggests that some lamb supply is being diverted away from the domestic market to higher paying export markets.

While overall lamb export volumes are holding up, performance across key export regions has been mixed. Higher export volumes to Europe (+19 per cent) and Asia (+15 per cent) have offset lower volumes to north America (-12 per cent) and Middle East (-22 per cent).

Uneven export performance illustrates that demand for Australian lamb is being negatively influenced by historically high price levels and a higher $A with processors and exporters reporting some price fatigue from customers in key import markets.

This suggests that demand for sheepmeat is likely to be compromised by a second round of price peaks in winter 2026.

In response to the price and supply outlook, the local processing sector is preparing for operational adjustments through the coming autumn and winter. This includes reducing operating days or shifts and extending winter shutdown periods.

Some processors are responding to the outlook by offering supply contracts for autumn and winter. In mid-February, Gundagai Meat Processors said it would offer a 10-week forward price grid at a $10.70/kg dw base rate, with producers also being paid half of any upside on their spot grid at the time of processing.

In addition to managing lower supply, the industry is also facing some trade access headwinds such as moves to impose some restrictions on US lamb imports.

US Sheep industry agitates for tariffs on Australian and New Zealand Lamb

Parts of the US domestic sheepmeat industry are agitating to increase the tariffs on imports from Australia and New Zealand to 30 per cent(pc) or impose a tariff rate quota to protect its domestic industry from imports.

The US sheep industry has been in long-term decline with imports replacing domestic production. The US lamb crop has shrunk from 3.6 million head in 2010 to 3 million head in 2025. US domestic lamb prices are around 15 per cent higher than last year.

In November, the American Sheep Industry Association (ASI) formally requested US Trade Representative (USTR) Jamieson Greer investigate whether lamb imports are harming the domestic industry. There has been no formal announcement by the US administration of an investigation as per the normal process, whether the current Administration adheres to this is another matter.

In late January, Republican Senator Mark Amodei, introduced legislation that imposes a 30pc tariff on sheep and lamb products from Australia or New Zealand. His two-page bill says "the president shall impose a 30 per cent duty on each sheep product and lamb product originating from Australia or New Zealand" within 30 days of the bill's enactment.

The tariff would be "in addition to each other applicable duty", meaning it would rise to 40 per cent when combined with the current 10 per cent tariff.

Tariffs and high lamb prices create headwinds for US lamb exports

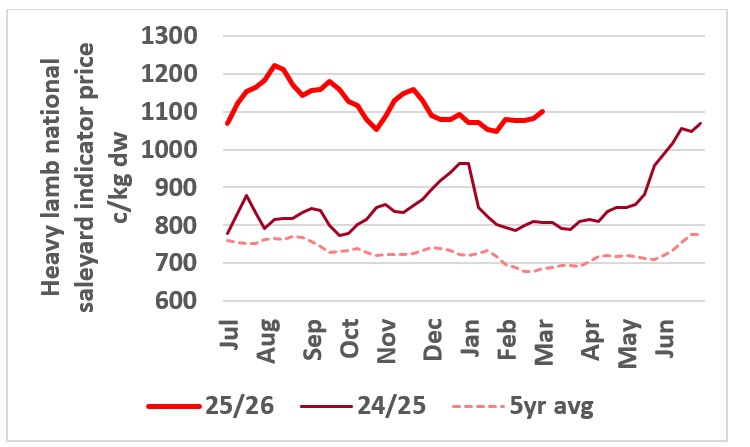

Heavy lamb prices have been nudging record levels at saleyards throughout New South Wales with a pen of extra heavy lambs selling to $472/head at Wagga recently followed by $495/head at Griffith as export processor demand lifts ahead of the peak US Greek Easter demand period.

This chart shows the national saleyard indicator prices for heavy lambs in 25/26 vs 24/25 and 5-year average. Source: MLA.

This chart shows the national saleyard indicator prices for heavy lambs in 25/26 vs 24/25 and 5-year average. Source: MLA.

Heavy lamb markets are well supplied given the increased level of lamb feeding due to high meat protein values and relatively cheap barley.

The Griffith lambs were ‘as long as battleships’ and estimated around 47kg carcass weight with a neat skin valued at around $7 to $8, pricing them around $10.50c/kg dw.

Australian lamb exports to the US and correspondingly local heavy lamb demand, peaks in February/March ahead of US Easter and Greek Orthodox Easter, when US lamb consumption spikes. Australian exporters ship product 4 weeks ahead, so US export volumes generally peak in February/March. Easter this year is 5 April and Greek Easter falls on 12 April.

However, while we are enjoying some seasonal strength in heavy lamb demand, there is evidence that the 10 per cent US tariff and higher imported lamb costs are slowing sales.

Total US lamb imports in the past four weeks (ending February 21) were 7,403 tonnes, down 6 per cent or 480 tonnes compared to the same period in 2025. Imports from Australia accounted for near 72 per cent of the imported volume and were 5,311 tonnes, 550 tonnes (-9.4 per cent) lower than last year.

Demand is also shifting towards lower cost items. As an example, square cut lamb shoulders are up 28 per cent in value compared to a year ago. While specific lower value items might be increasing, prices for imported lamb are all over the place with prices for boneless legs lower than a year ago.

US Treasury Secretary Scott Bessant said that President Donald Trump’s recently announced 15 per cent global tariffs will likely be implemented soon which will raise US tariffs on sheepmeat from 10 to 15 per cent.

Outlook: US tariffs and higher imports costs are affecting demand for Australian sheepmeat in the US market. Supply tightness is likely to keep heavy lamb values in the $11 to 12/kg dw range during winter, however, consumer resistance to higher prices and the impact on export returns of a higher $A will most likely limit further advances beyond this range.

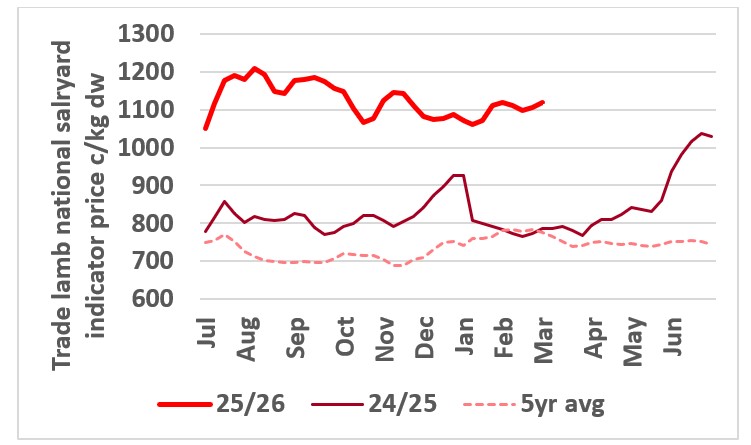

Supply tightness push trade lambs higher but consumer resistance will limit further gains

Lower supply and increased export market focus has forced domestic retailers to compete for supply which has kept the pressure on trade lamb values.

At the retail counter, lamb values are around 30 to 40pc higher than this time last year, impacting domestic consumption.

Helping to support trade lamb values is competition from feeders looking to secure trade lambs 20 to 22kg to feed to export weights 26 to 30kgs through autumn winter when lamb supplies tighten.

This chart shows the national saleyard indicator prices for trade lambs in 24/25 vs 25/26 vs 5year average. Source: MLA.

This chart shows the national saleyard indicator prices for trade lambs in 24/25 vs 25/26 vs 5year average. Source: MLA.

Outlook: Tight supplies should keep trade lambs around the current trading range with consumer resistance to higher price limiting further gains.

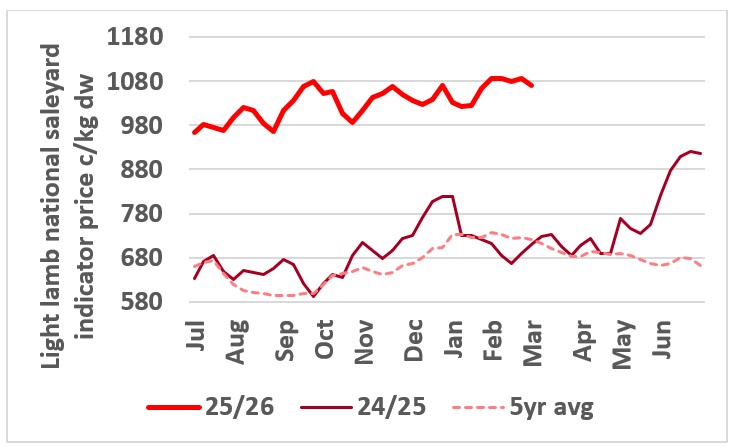

Light lamb export markets look difficult but restocker and feeders will support prices

Demand for sheepmeat from the Middle East for Ramadan has underpinned strength in light lamb values with these performing the best of any lamb category over the past few months. There has also been some domestic processors active on these lighter categories (to try and lower the buy price to meet stretched domestic customer budgets) and some competition from the feeding sector.

While demand has been solid, recently export demand for light lamb has been impacted by the US/Iran conflict that has shutdown air freight and shipping routes to the Middle East and has seen a dramatic increase in freight costs and exporting risks into the region. The Middle East is an important export market for Australian sheepmeat taking around 10 per cent of total exports, mainly light lambs under 20kgs which are processed and air freighted in whole chilled carcase form (mk bag trade).

Prices for lambs under 20kg carcase weight have run into some trouble at isolated markets owing to a pullback in export demand but tight supplies and strong restocker and feeder demand are expected to mitigate any ongoing impacts.

This chart shows the national saleyard indicator prices for light lambs in in 24/25 vs 25/26 and 5-year average. Source: MLA.

This chart shows the national saleyard indicator prices for light lambs in in 24/25 vs 25/26 and 5-year average. Source: MLA.

Outlook: Prices will be supported at the upper end of the recent trading range as restockers and feeders out compete the processing sector. Lamb supplies will be diverted to markets outside the Middle East if conflict is prolonged with high cost, transport difficulties and heightened risk making supplying this market difficult.

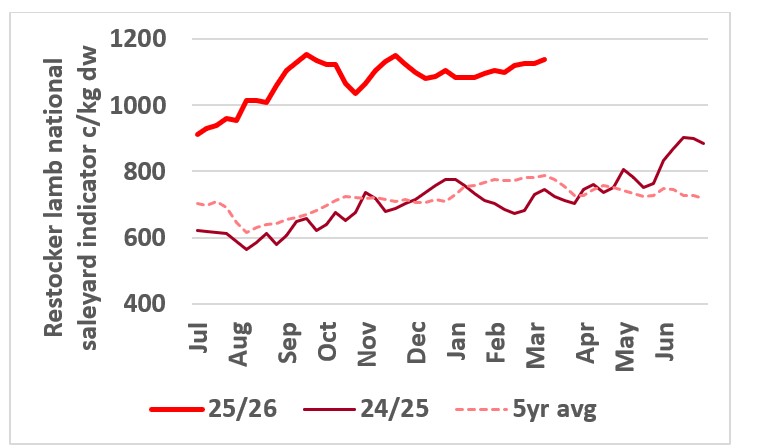

Rain breathes life into restocker market and creates options for producers

Widespread and significant rainfall across major sheep producing regions in central and southern Australia will generate a flush of feed and allow producers to rebuild flocks after three very tough years.

Pastoral areas that have been a major source of supply for the processors and southern feeders will effectively close the gate and rebuild numbers, exacerbating the seasonal tightening in supply this autumn/winter. In the past year, strong prices and a lack of pasture have seen producers offloading lambs early rather than carrying them through to spring and selling them off shears. Some may still opt to offload lambs early to take advantage of the higher prices on offer but lamb availability from these areas is likely to be well down.

For mixed farmers, fodder crops such as oats, vetch and red wheat are likely to be planted while the rain will germinate weeds and self-sown crops and promote pasture growth ahead of the winter. Whether people buy in more stock to value-add pasture remains to be seen, but there are plenty of sheep in containment pens and this rain will allow at least some to go on to paddock feed.

Restocker values will lead lamb markets higher leading into winter as producers restock. Recently Elders held a store lamb sale at Muchea in WA, where 19,500 lambs were offered ranging from 35 to 54kg liveweight to average 43 to 44kg and sold to an average of $225/head.

Of the offering 10,000 were trucked back East with local WA processors, exporters and feeders unable to compete. Recently we have heard rates as high as $13/kg lw being paid for store lambs while at the Wycheproof store sale ‘not pretty’ southern Riverina light merino wether lambs sold to $7/kg lw.

This chart shows the national saleyard indicator for restocker lambs in 24/25 vs 25/26 and 5-year average. Source: MLA.

This chart shows the national saleyard indicator for restocker lambs in 24/25 vs 25/26 and 5-year average. Source: MLA.

Outlook: Restocker categories will lead the lamb market over the next few months as producers across the central and south-eastern regions look to rebuild numbers.

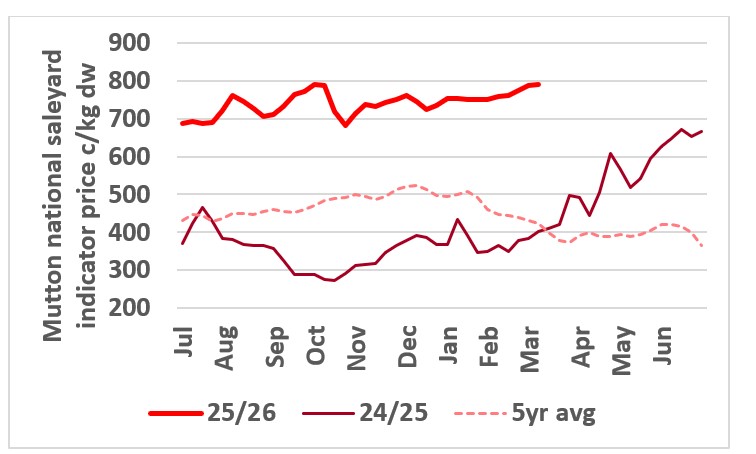

Mutton rocket higher

Owing to sharply lower mutton slaughter (-29 per cent) and lower production, prices paid by processors for mutton has soared in recent weeks as works seek to fill slaughter schedules.

The industry will adjust to lower supplies through autumn and winter by reducing capacity.

Already we are seeing the impact on restocker demand from the dramatic improvement in conditions through key sheep regions with the lift in values for sheep almost immediate.

This chart shows the national saleyard indicators prices for mutton this year vs 23/24 and 7-year average. Source: MLA.

This chart shows the national saleyard indicators prices for mutton this year vs 23/24 and 7-year average. Source: MLA.

At the recent Wycheproof store sheep sale, young merino ewes scanned in lamb to a merino ram sold to $400/head while merino ewes to a terminal sires made $360 to 370/head. These prices seem reasonable and have upside if their progeny remain around current elevated levels. For breeders and mixed farmers, the Merino wool and slaughter lamb combination is significantly better than many other per hectare returns which should see a firm move back to rebuilding flocks.

Restockers who look to the pastoral country for replacement ewes may be hard-pressed to find alternative sources as the flock rebuilds, particularly if lamb prices stay high.

Outlook: A pickup in restocker activity will ensure mutton prices remain at historic highs through autumn and winter.

Goat supplies to tighten with rain across pastoral areas

With the tightening in sheep and lamb supplies since mid-last year, goats have become a viable alternative for abattoirs to help fill slaughter schedules for small stock processors. Unlike lamb and mutton, the goat price hasn’t fully bounced back from the price slide in the spring of 2023, making them a viable alternative for export processors.

Goat values started to climb last year but are still 40 to 50 per cent behind the price trend line of quality lambs. As an example, goat prices averaged $6/kg dw well behind trade and heavy processing lambs around $11/kg dw.

The national goat kill went as high as 103,000 head per week in late spring, which was also influenced by the seasonal turn-off of goats and drying conditions across pastoral country. With recent rain throughout pastoral regions. Goat supply is likely to again tighten with slaughter rates in recent weeks pushing back toward 60,000 head per week, a 3-year low.

Export performance has been mixed, with exports lower overall in line with lower slaughter but picking up some pace heading towards the peak demand season in north America. Australia is effectively the only supplier of imported goat meat for north America, with this market accounting for about 60 per cent of all Australian goat meat exports (lower exports to the US offset by big gains in Canada). Goat exports to Asia have more than halved with China virtually ceasing imports.

Outlook: The recent rain will mean that goat availability will shorten, keeping prices around current levels but placing downward pressure on slaughter and exports.

From the rails

Read what Elders livestock representatives from around Australia are saying about the markets in their regions.

“At Tamworth, lamb numbers were back in a mixed yarding with odd pen of heavy weight lambs and fair numbers of trade weight lambs. Lighter restocker lambs were well supplied. A full field of buyers were operating in a solid market. Trade lambs were $14 dearer with the 20kg to 24kg lambs ranging from $221 to $274/ head. Heavy weight lambs were up to $16 dearer with 24kg to 30kg lambs selling from $231 to $335/head while the extra heavy weights sold to $376/head. Young lambs to the restockers were up to $30 dearer with the restockers paying from $84 to $275/head. Hoggets sold to $280/head.”

“There was a decent sized yarding of mostly good quality mutton yarded where most grades were $12 dearer. Merino ewes sold from $120 to $269/head while cross bred ewes made from $156 to $335/head. Merino wethers sold from $185 to $200/head.” - Mark Atkin, Branch Manager, Guyra/Armidale.

“Our market was very strong this week with feeders active on anything outside of heavy weights pushing values to north of $12/kg. The big change in our industry over the past 35 years has been the development of a professional feeding industry which is providing competition for the processors. Even if they aren’t turning a dollar they need to keep operating to retain staff and utilise their investments. We have had a standing order for feeder lambs for South Australian feedlots for most of the year which has underpinned our market.”

“Quality was good with trade and heavy weight lambs very well supplied. The light lambs available were sort after by restockers, with little going to processors. All the regular buyers were operating in a strong market. Trade, selling from $248 to $298/head. Heavy lambs were steady, lambs 24kg to 26kg sold from $275 to $316, and lambs to 30kg, $315 to $347/head. Carcase prices averaged between 1180c and 1240c/kg dw. Light lambs to restockers sold to $266 and heavy hoggets reached $280/head.

“The mutton yarding was mixed quality, but prices remained strong. Merino ewes sold from $148 to $237, and crossbred ewes, $152 to $306/head. Merino wethers sold from $120 to $188, and heavy Dorper rams sold to $210/head. Most sheep sold in the range of 840c to 880c/kg dw.” - Ben Emms, Livetsock Manager, Emms Mooney.

“At Wagga. lamb numbers rose following last week’s positive market. Quality remained excellent, with a good percentage grain-fed trade and heavy lambs. This week, however, there was a noticeable tail in the offering of secondary lambs. Despite this, restockers remained undeterred by the planer types. Feedlots dominated the trade weight categories, prompting processors to step up their bids on recently shorn second cross lambs.”

“Trade lambs saw robust demand, largely supported by feedlots. Lambs in the 21 to 24kg weight range, well-suited for processors, sold between $251 and $296, averaging 1193c/kg dw. In the same weight category, lambs destined for feeding fetched between $238 and $290.

“Merino trade lambs were in short supply, yet those that were offered sold exceptionally well, with prices ranging from $218 to $290/head. Lightweight lambs aimed at restockers attracted strong interest, although the Dorper portion influenced price averages. Restocking lambs traded between $112 and $240 per head.

“Heavy export lambs, on the other hand, lacked the weight seen in the previous week. Lambs weighing 26 to 30kg sold firmly with all processors operating in this weight category, prices ranged from $315 to $353/head to average 1159c/kg dw. For extra heavy lambs exceeding 30kg, competition intensified, leading to sales between $348 and $448/head.

“A very mixed yarding of mutton saw the buying intensity of last week slip and prices eased $6-$27/head to average 820 to 849c/kg dw. Heavy sheep made from $220 to $310 to average 778 to 856c/kg dw. - John Crawford, Branch Manager Central and Southern NSW.

| NSW sheepmeat saleyard indicatorsc/kg dw | ||||

| 12 Mar 26 | +/- week | +/- month | +/- year | |

| Lambs | ||||

| Heavy | 1107 | 1110 | 1087 | 805 |

| Trade | 1177 | 1167 | 1110 | 810 |

| Light | 1095 | 1080 | 1065 | 742 |

| Restocker | 1157 | 1154 | 1124 | 715 |

| Merino | 1051 | 1023 | 968 | 670 |

| Mutton | 831 | 820 | 773 | 429 |

Source: MLA

"Central and northern Victoria has generally had 50mm and up to 100mm of rain if you got under a storm. Heavy lambs in the $12/kg dw and mutton over $10/kg with light mutton making $150-170/head."

"Ararat back to 3 day kills which gives you an indication of how hard it is to find supply.

"Store sheep sale at Wycheproof, young merino ewes scanned in lamb to a merino ram $400/head. Merino ewes to a terminal ram $360 to 370/head and light merino wether lambs that were not pretty sold to $7/kg lw.

"At Ballarat, numbers lifted with lambs coming off feed presenting in exceptional condition across the lead of the heavy export and heavy trade categories. Quality through the light and trade weights was more mixed. Most of the usual buying group attended which saw strong competition and increased bidding intensity across all weights and grades.

"Store lambs are still in high demand, selling $5 to $10 dearer, light and medium trade gained to $8 to $12, while heavy trade were also in demand, gaining $10 to $14/head. Extra heavy export lambs sold to a top of $427 and sold $12 to $15 stronger with some sales to $30/head dearer.

"Store lambs back to the paddock made $130 to $234, while lambs to feed on made $225 to $308/head. Light trade made from $215 to $226, Medium trade made from $233 to $278 and heavy trade sold from $256 to $318/head, to average 1160c to 1220c/kg dw. Heavy lambs 26 to 30kg sold from $298 to $355 and over 30kg lambs made from $350 to $427/head to average 1090 to 1140c/kg dw. Crossbred hoggets sold well, selling from $147 to $320 and the Merino’s made from $143 to $240/head.

"Sheep numbers increased with all the usual buyers on the rail in a stronger market throughout the yarding with sales $10 to $20/head dearer. Merino wethers selling from $154 to $306 to average 850c to 950c/kg cwt". - Nick Gray, State Livestock Manager Victoria/Riverina.

| Victorian sheepmeat saleyard indicators c/kg dw | ||||

| 12 Mar 26 | +/- week | +/- month | +/- year | |

| Lambs | ||||

| Heavy | 1121 | 1076 | 1083 | 818 |

| Trade | 1157 | 1119 | 1114 | 784 |

| Light | 1137 | 1105 | 1116 | 772 |

| Restocker | 1193 | 1157 | 1151 | 754 |

| Merino | 1086 | 988 | 1028 | 684 |

| Mutton | 828 | 777 | 746 | 443 |

Source: MLA

“We just had 10 days of rain through the north of South Australia. Our north-west pastoral country had 4 to 6 inches. They shear at this time of year, and we normally draw a lot of supply from these areas, so that’s going to be up in the air moving forward.”

“Port Augusta through to Glendambo and out north of Broken Hill had 10 inches and the dry areas to the south have started to fill in through Pooncarie, Mildura and Yunta.

“Western Eyre had the biggest February rainfall since 1938. So significant rainfall through the state to north of Broken Hill is going to impact supply. Producers in these areas will use this opportunity to build numbers back up.

“Sheep and lamb prices are firming with a lift in restocking activity. Supply is expected to be very, very tight in our patch for the foreseeable future. Most significant development is in breeding sheep. On the box scanned in lamb merino ewes to British ram $400/head with August/September wool.” - Damien Webb, Livestock Sales Manager SA.

| SA sheepmeat saleyard indicators c/kg dw | ||||

| 12 Mar 26 | +/- week | +/- month | +/- year | |

| Lambs | ||||

| Heavy | 1059 | 1038 | 1011 | 765 |

| Trade | 1065 | 1059 | 1053 | 750 |

| Light | 1042 | 1103 | 998 | 761 |

| Restocker | 1074 | 886 | 1233 | 676 |

| Merino | 1067 | 971 | 985 | 682 |

| Mutton | 741 | 734 | 727 | 389 |

Source: MLA

“Not a lot of change. Sheep are very strong $7.20 to 7.50/kg dw. You can almost name your price given lack of numbers. A few lambs coming out of feedlots, which we expected through February/March. Price still holding around $10.30/kg dw.”

“Demand for stores is incredible north of $5/kg lw. No weight restrictions they are taking anywhere between 30 to 50kgs at around $5.20/kg lw. Focus for us will be scanned in ewes that will start running around mid-March.” - Wayne Peake, Livestock Sales Manager WA.

| WA sheepmeat saleyard indicators c/kg dw | ||||

| 12 Mar 26 | +/- week | +/- month | +/- year | |

| Lambs | ||||

| Heavy | 985 | 985 (n/c) | 1047 (-62) | 728 (+257) |

| Trade | 949 | 967 (-18) | 1091 (-142) | 636 (+313) |

| Light | 942 | 918 (+24) | 799 (+143) | 524 (+418) |

| Restocker | 996 | 968 (+28) | 1197 (-201) | 399 (+597) |

| Merino | 820 | 708 (+112) | 870 (-50) | 436 (+348) |

| Mutton | 644 | 656 (-12) | 642 (+2) | 224 (420) |

Source: MLA

“There was +10mm of rain for northern Tassie, 3 to 5mm in the south with another 10mm forecast for this week. This has turned the market around over the past fortnight.”

“There was intense competition in sheepmeat markets last week. Lambs $10/kg dw direct to works but trades $9.80 to 11.20/kg dw at the yards and heavy types $11.20 to 12.90/kg dw. Processors are struggling to fill slaughter schedules. Mutton gained another $20 to 30/head easily this week, the lighter end $8.20 to 10/kg dw and the heavy end $7.80 to 10/kg dw with numbers starting to shorten up.” - Gavin Coombe, Livestock Manager Tasmania.

| TAS sheepmeat saleyard indicators c/kg dw | ||||

| 12 Mar 26 | +/- week | +/- month | +/- year | |

| Lambs | ||||

| Trade | 1072 | 1027 | 973 | 770 |

| Restocker | 992 | 1052 | 972 | 540 |

| Mutton | 793 | 777 | 783 | 443 |

Source: MLA

“There is no flooding around Longreach now, however, we are expecting some flooding when the water comes down the River. We are still looking for some runoff rain to fill on farm storages. Anywhere north of Muttaburra is a write off for now in terms of getting access to stock.”

“Draw a line from Longreach to Charleville and across to Warwick and anywhere south needs more rain.

“We have sheep stockpiled ready to go, mainly dry ewes and lambs that have been classed out. We sent 8 decks of sheep to Forbes last week and have been sending stock to South Australian for the feedlots there.

“There are sheep moving because they require management and with crutching, shearing and scanning ongoing there are always bits and pieces available for sale. The hardest part is getting full consignments; we may need to make 3 or 4 stops.” - Tim Salter, Branch Manager, Western and Central Queensland.

| Queensland sheepmeat saleyard indicators c/kg dw | ||||

| 12 Mar 26 | +/- week | +/- month | +/- year | |

| Lambs | ||||

| Heavy | 1061 | 963 | 1045 | 738 |

| Trade | 995 | 1005 | 1059 | 636 |

| Light | 919 | 1022 | 1031 | 570 |

| Restocker | 861 | 647 | 980 | 568 |

| Mutton | 618 | 613 | 662 | 167 |

Sources: Price data reproduced courtesy of Meat & Livestock Australia Limited.

*Disclaimer – important, please read:

The information contained in this article is given for general information purposes only, current at the time of first publication, and does not constitute professional advice. The article has been independently created by a human author using some degree of creativity through consultation with various third-party sources. Third party information has been sourced from means which Elders consider to be reliable. However, Elders has not independently verified the information and cannot guarantee its accuracy. Links or references to third party sources are provided for convenience only and do not constitute endorsement of material by third parties or any associated product or service offering. While Elders has exercised reasonable care, skill and diligence in preparation of this article, many factors including environmental/seasonal factors and market conditions can impact its accuracy and currency. The information should not be relied upon under any circumstances and, to the extent permitted by law, Elders disclaim liability for any loss or damage arising out of any reliance upon the information contained in this article. If you would like to speak to someone for tailored advice specific to your circumstances relating to any of the matters referred to in this article, please contact Elders.